First Look at Cannabis Consumer Retail Trends in Nevada

Marijuana Industry NewsNevada January 24, 2019 MJ Shareholders 0

You might think that what happens in Vegas dispensaries stays in Vegas dispensaries. And surely some pot-shop shenanigans never do leave the Silver State’s biggest city. But the volume of flower sales? Market share for vapes? What kind of edibles Nevadans consume? That data and much more now is no longer secret, as cannabis market research firm BDS Analytics this month launches its data platform detailing retail consumer trends across Nevada — everything from the average price paid for a pre-rolled joint to the popularity of tinctures.

Let’s take a look at how the gambling-grooving residents and tourists of the nation’s 36th state spend their money in Nevada’s 60 dispensaries.

State residents endorsed legal adult-use sales during the 2016 election, and less than two months later, on Jan. 1, 2017, dispensaries began selling cannabis products to anybody 21 or older. In this report, we closely examine trends between July and October of 2018, comparing these four months to the same months during 2017. We also look at sales for all of last year through October, without comparing the data to 2017.

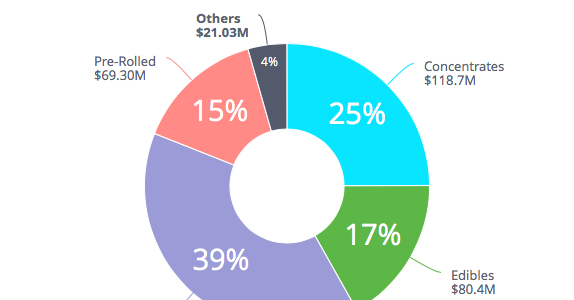

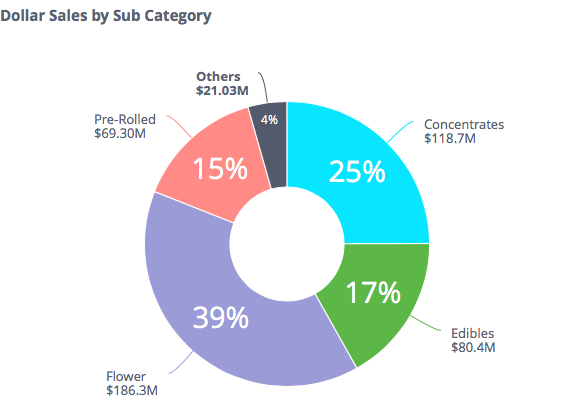

A breakdown of sales for 2018 through October.

First of all, the basics. For 2018 through October, people spent $476 million on cannabis products. How did they divide the cannabis pie? Thirty-nine percent of sales went towards flower, concentrates commanded 25 percent, and edibles hit 17 percent. Pre-rolls, which in other states tend to harness between 5 and 8 percent of sales, were much more popular in Nevada, where they capture 15 percent of cannabis sales. Nice work, blunts.

Since Nevada is a mining state, let’s honor the legacy and do some deep digging.

Flower

Sales between July and October reached $76 million, which represents growth of 5.2 percent compared to the same period in 2017. The average retail price during the period in 2018 was $11.80, which is down about 10 percent from the same period during 2017. Flower remains pricey in Nevada — more expensive than in California, Colorado and Oregon. But as in the other states, the price trend leads down.

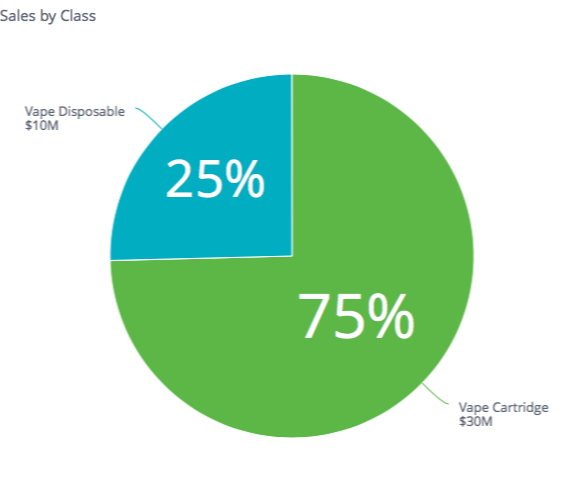

Disposablel vapes are popular in Nevada.

Concentrates

Consumers dropped $50.1 million on concentrates during the four-month period under review, which represents growth of 35 percent compared to the same period in 2017. And just as it is in all other states, vapes rule. In Nevada they own 78 percent of the concentrates market, compared to 6 percent for oils and 5 percent for shatter and wax respectively. Interestingly, disposable vapes in Nevada perform quite well, harnessing 25 percent of vape sales. Disposables in California, on the other hand, represent just 13 percent of vape sales, and that number is even lower in Colorado and Oregon. Disposable vapes are about as discrete as you can get — many are about the size of a cigarette. Could their popularity in Nevada be tied to the state’s heavy tourism, with so many consumers spending time in hotels? Quite possibly.

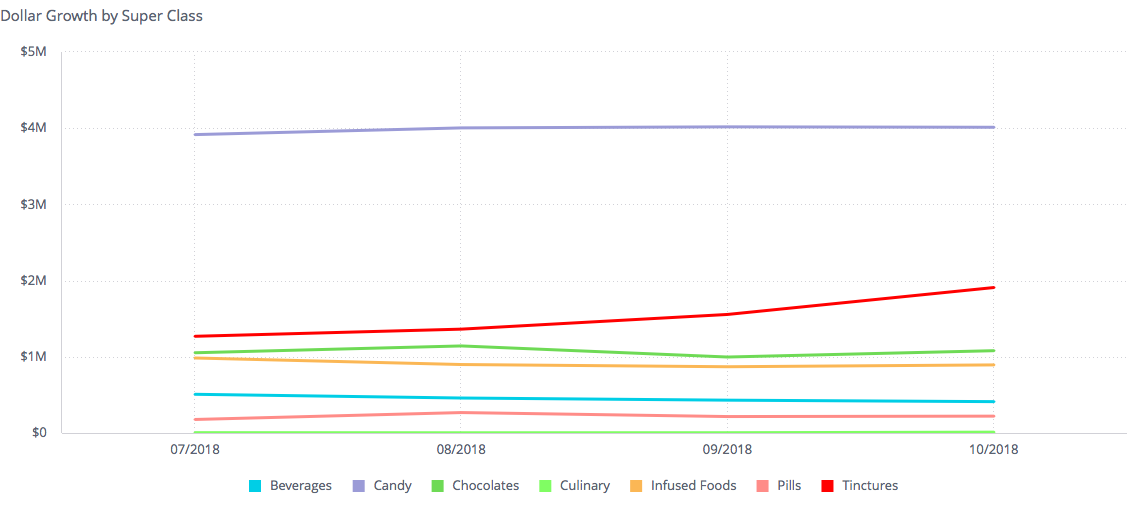

Tinctures are rising.

Edibles

Sales of $33 million during the four-month period mark healthy growth — 32 percent, compared to the same period in 2017. California’s edibles growth during the period was just 18 percent.

Candy is the market leader in Nevada, as in all states, with 49 percent of sales. The big mover within edibles in Nevada, though, is tinctures. Dollar sales expanded by 177 percent during the period, compared to 35 percent for candy and 5 percent for chocolates.

We will have much more to cover in this dynamic and fast-growing market in coming months and years. But for now, at least, it looks like a wide range of entrepreneurial gambles are paying off, from Las Vegas to Reno to more remote corners of the gigantic desert state.

MJ Shareholders

MJShareholders.com is the largest dedicated financial network and leading corporate communications firm serving the legal cannabis industry. Our network aims to connect public marijuana companies with these focused cannabis audiences across the US and Canada that are critical for growth: Short and long term cannabis investors Active funding sources Mainstream media Business leaders Cannabis consumers

No comments so far.

Be first to leave comment below.