Psychedelic Drug Industry Report Card For 2021

Marijuana Stocks, Finance, & InvestingUncategorized August 31, 2021 MJ Shareholders

- Excellent progress in drug development, IP development, clinic operations and corporate development

- A more mixed year in terms of reform of drug laws and stock price performance

Psychedelic Stock Watch has spent recent weeks focusing on the potential of psychedelic medicine. There were two reasons for this.

First, the Mental Health Crisis, which was already a global pandemic, has been spiraling out of control. The intense stress caused by Covid-19 lockdowns has been taking a tremendous mental health toll on all demographics of society.

Secondly, our perspective on the commercial potential of psychedelic medicine continues to become increasingly bullish.

- Identifying the enormous treatment populations that could/can benefit from psychedelic medicine.

- Seeing the science behind psychedelic medicine get even more exciting as we start to learn how psychedelics can (literally) “rebuild broken brains”.

- Watching the number of research/commercial opportunities for psychedelic drugs continue to mushroom (pun intended).

Now we’re turning our attention to assessing the industry itself. Instead of waiting until year-end, we’re compiling our 2021 report card now.

After a quiet summer (in terms of stock performance), many investors will be getting more serious about stocks. This will give them some assistance in rebalancing their portfolios as we head into the last third of 2021.

And there is already a lot to report for this year.

Drug development: B+

In assessing the psychedelic drug industry, a primary focus for investors is drug development. As we reach the end of August, there has already been enough progress for the industry to score a “B+” in this category.

Leading the way, the Multidisciplinary Association for Psychedelic Studies (MAPS) announced very successful results for its Phase III clinical trial using MDMA-assisted therapy to treat PTSD.

- 88% “experienced a clinically meaningful reduction in symptoms”. (In comparison, two-thirds of veterans receiving treatment for PTSD from the Department of Veterans Affairs reports no benefit from treatment.)

- 67% of participants “no longer qualified for a PTSD diagnosis”, i.e. they were cured

A revolutionary improvement on the existing standard of care for PTSD. Vancouver-based Numinus Wellness (CAN:NUMI / US:LKYSF) has been a partner with MAPS in conducting this Phase III trial.

Right behind MAPS, Compass Pathways (US:CMPS) announced the completion of its Phase IIb clinical trial of a psilocybin-assisted therapy to treat Treatment-Resistant Depression (TRD). Results from the study are expected by year-end.

Compass also announced receiving two more U.S. patents in support of this research.

Atai Life Sciences (US:ATAI), the partner/parent of Compass Pathways has a total of three R&D programs in or commencing Phase II clinical trials among its eleven research partners.

MindMed Inc (US:MNMD / CAN:MMED) announced news on three of its many Phase II and Phase I clinical trials. Project Lucy moved closer to commencing its Phase IIb study, an LSD-based therapy to treat anxiety disorder.

MindMed also announced commencing a Phase I clinical trial on DMT and the first Phase I clinical trial combining LSD and MDMA.

Cybin Inc (US:CYBN / CAN:CYBN) announced it’s close to launching its Phase IIa clinical trial of a psilocybin-based therapy for Major Depressive Disorder. The company is also actively expanding its drug pipeline and has now filed a total of 16 patent applications in support of its research.

Seelos Therapeutics (US:SEEL) announced Part 2 of its Phase IIa clinical trial of a ketamine-based treatment for ALS (Lou Gehrig’s disease).

Awaken Life Sciences (CAN:AWKN / IS:AWKNF) announced the acquisition of IP from a completed Phase II a/b clinical trial of a ketamine-based treatment for alcohol use disorder, with plans to move to a Phase II trial.

Mydecine Innovations Group (CAN:MYCO / US:MYCOF) announced it is commencing its Phase IIa clinical trial of a psilocybin-based therapy to treat PTSD. Mydecine also recently announced a new R&D partnership with Johns Hopkins University to tackle the enormous nicotine addiction market.

Numinus Wellness commenced a Phase I clinical trial of its natural psilocybin extract.

A lot of drug R&D progress for the industry already this year. With planning underway for numerous Phase I, Phase II and even Phase III clinical trials, we can expect the industry’s progress on drug development to continue to accelerate.

Mental health clinics: B

With roughly two billion treatable mental health disorders globally, there is obviously immense blue-sky potential for the psychedelic drug industry in developing and operating mental health treatment clinics.

With lots of news announced on this front as well in 2021, the industry earns a solid “B”. That grade might have been higher if the bar hadn’t already been set high in terms of drug development. Several public companies have released significant news in clinic development in 2021.

NASDAQ-listed Field Trip Health (US:FTRP / CAN:FTRP) is the best-known public company with respect to clinic operations. Field Trip has opened two more mental health clinics in its North American network this year, with five additional clinics under construction.

Another investor favorite with deep operations in mental health clinics is Numinus Wellness. In 2021, Numinus has bolstered its clinic operations with (first) the acquisition of Montreal-based Mindspace Wellbeing and more recently the Neurology Centre of Toronto.

Those acquisitions will not only provide a substantial revenue stream for Numinus but will also enhance its drug R&D efforts.

Another major player in mental health clinics within the psychedelic drug industry is Novamind Inc (CAN:NM / US:NVMDF). Novamind already has the largest revenue base in mental health clinics via its Cedar Psychiatry network. Novamind is in the progress of doubling that network from 4 to 8 locations, and recently announced the opening of the 5th clinic outlet.

Levitee Labs (CAN:LVT), a new Canadian-based pubco, recently closed on the acquisition of 5 addiction clinics in Alberta.

Awaken Life Sciences has announced the opening of its 2nd UK clinic.

The overall footprint of these public companies in mental health treatment has more than doubled already this year. With enormous blue-sky potential and many new clinics in planning (or to be acquired via acquisition) we can expect expansion of mental health treatment clinics to also continue to accelerate.

Other IP development: B+

With a multitude of psychedelic drugs and an even greater multitude of treatment markets being targeted by the psychedelic drug industry, there are enormous opportunities in IP development beyond drug patents.

Drug synthesis and drug delivery systems alone provide countless opportunities for IP development. Numerous public companies are active on this front and a great deal of news has been announced in 2021 advancing this research.

More specifically, Psychedelic Stock Watch has been focusing on digital therapeutics platforms. This IP got our attention when Mindstrong Inc, a private company, completed a $100 million financing round solely to advance its own digital therapeutics platform.

With the incorporation of sophisticated AI, digital therapeutics is poised to add significant gains in both efficiency and efficacy to healthcare, in general. Mental health treatment, in particular, stands to enormously benefit from the introduction of these digital platforms.

Many of the public companies in the psychedelic drug industry are already working on these platforms or have plans to add digital therapeutics to their business models. Three of the pubcos have announced significant news on this front in 2021.

MindMed announced the acquisition of HealthMode, a “leading machine learning digital medicine company”.

Mydecine has announced the launch of MindLeap “Version 2.0”.

Most recently and perhaps most significantly, Mind Cure Health (CAN:MCUR / US:MCURF) has announced it is ready to deploy its own iSTRYM digital therapeutics platform. MINDCURE is expecting to begin full commercial deployment in Q1 2022 and forecasting penetration to 150 clinics in Canada, the U.S. and Europe by the end of 2022.

Drug development and mental health clinics will continue to lead the way in terms of overall growth opportunities in the psychedelics space. However, investors would be well-advised to also become familiar with (and invested in?) the next-generation IP being developed to support psychedelic medicine.

Corporate development: A

If investors did nothing but stare at the (generally stagnant) price charts of psychedelic stocks in 2021, they would never guess that the industry has been moving full-speed ahead on corporate development. A ton of major news to cover here.

Atai Life Sciences, the industry leader by market cap, went public in June on the NASDAQ. After raising $157 million earlier in the year with its Series D financing round, ATAI announced it was raising as much as $246 million more for its IPO.

Atai’s most prominent research partner, Compass Pathways, raised another $154.8 million in May.

MindMed Inc also made its NASDAQ debut, uplisting in April. MindMed continued its own aggressive capital-raising, adding roughly ~USD$100 million to corporate coffers. This earned MindMed a spot on the Russell 3000 index.

Seelos Therapeutics, also NASDAQ-listed, raised $64.5 million earlier this year. Seelos then announced its own addition to the Russell 2000 and 3000.

Ireland-based GH Research (US:GHRS) also went public on the NASDAQ this year. That was after raising $125 million in its final private financing round.

Field Trip Health was the other psychedelic stock to obtain a new NASDAQ listing this year. Field Trip uplisted at the end of July. That was after closing a CAD$95 million bought-deal financing, the largest single Canadian-based public offering.

Cybin Inc didn’t uplist to the NASDAQ, but it did uplist to the NYSE American. Cybin has also inked two significant partnerships. Early this year, Cybin announced a drug development deal with Catalent, a heavyweight in the pharmaceutical industry. Then came a research collaboration agreement with Greenbrook TMS, one of the leading providers of mental health services in the U.S.

Cybin also found time to raise more capital and set up an Irish subsidiary for psychedelics operations.

In addition to this, roughly a dozen other psychedelics-based companies went public on smaller exchanges. Numerous additional smaller financings have been closed this year to fund operations of the smaller players.

This is an enormous amount of corporate development in only eight months for an emerging industry less than two years old (in terms of public companies). Imagine how much busier this sector would have been with stronger stock performances.

Drug reform: C+

One of the few disappointments in the psychedelic drug industry is something beyond the control of these public companies: drug reform. Here it is governments that are receiving a mediocre letter grade.

To be sure, these has been some progress to date in 2021 on reform of psychedelic drug laws – but not enough.

In Canada, at the federal level Health Canada has been slowly-but-steadily opening up access to psilocybin-assisted therapy through the granting of special “exemptions” (from drug statutes), primarily as compassionate relief for terminal patients.

The federal government is signaling willingness to continue to expand access. But (as usual) the politicians are behind the people. In a mid-year poll, it was reported that 80% of Canadians simply want psilocybin legalized for medicinal use.

In the United States, progress was more limited. Yes, there was considerable movement at the state and local level to loosen drug laws and increase access to psychedelic drugs – at least via decriminalization.

However, one state (Washington) actually recriminalized psychedelic drugs after courts struck down a state drug law.

At the federal level, the dinosaurs of Congress voted by a 331-91 majority to prevent the federal government from even studying the benefits of psychedelic medicine. These senior citizens don’t want facts and science to get in the way of their anti-drug biases.

That disappointing vote drained any sense of optimism after the introduction of the “first-ever Congressional bill” to decriminalize all drugs.

We continue to live in a surreal world where (successful) formal clinical trials on the efficacy of psychedelic medicines continue to advance while archaic drug laws still ban psychedelics as substances with “no accepted medical use”. Legal perversion.

It may ultimately require court challenges to shock these politicians out of their anti-drug stupors and get them to move forward on meaningful reform of punitive and obsolete drug laws.

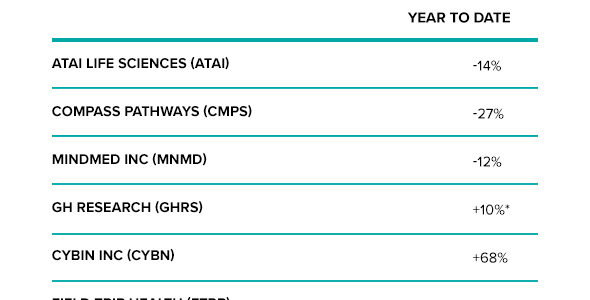

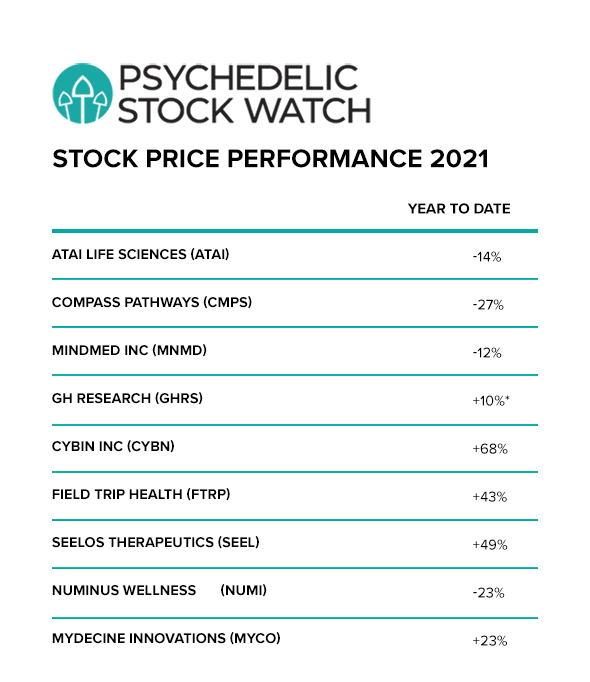

Stock performance: D

The only other area where the psychedelic drug industry didn’t earn a strong grade is the only other area outside the direct control of these companies: stock performance.

As investors in psychedelic stocks can attest to, most of these public companies have seen their share prices drift sideways-to-lower for most of the year.

The huge irony here is that (as noted above) the industry itself has made enormous leaps forward over the first eight months of 2021. However, with few exceptions these public companies have not been rewarded for their strong operational performances. In contrast, many of these same companies generated spectacular returns in 2020 – on the back of far less substantial news and corporate progress.

A look at the stock performance of the industry’s largest players gives investors a partial picture here.

(*) measured from closing price after 1st day of trading

A few winners have emerged this year. But most companies are currently well off of 2021 highs and gains have been much more modest than in 2020.

The picture is much less-rosy for smaller companies in the industry. While a few companies have made runs in 2021, none have been able to sustain momentum.

In an industry plagued by anemic trading volumes for most of the year, the smaller companies have (not surprisingly) suffered the most. Losses for some of the hardest-hit players exceed 50%.

The flip-side to this is that (as Psychedelic Stock Watch has previously reported) the industry has gotten ridiculously concentrated (by market cap), despite the increasing number of players.

Given the vast number of commercial opportunities in the sector, we see strong potential for this level of concentration to reverse over the longer term.

Summary:

For investors, whether evaluating a company or a sector, it’s often a glass half-full/glass half-empty equation.

In the case of psychedelic stocks, do investors look at the anemic trading volumes and mediocre price performance and turn their backs on these companies as “under-achievers”?

Or, do they look at the vast treatment populations in mental health, huge treatment markets and spectacular clinical results and see an incredible value proposition?

Are investors more influenced by the lack of progress in drug reform, or the major successes in corporate development?

For glass half-empty investors, these are highly speculative stocks that generally haven’t lived up to expectations (so far) in 2021.

For glass-half full investors, these valuations are a chance to still get in on effectively the ground floor of what could be the biggest investment opportunity in life sciences of this century.

DISCLOSURE: The writer holds shares in MindMed Inc, Cybin Inc, Numinus Wellness, Mind Cure Health, Novamind Inc, and Levitee Labs.

MJ Shareholders

MJShareholders.com is the largest dedicated financial network and leading corporate communications firm serving the legal cannabis industry. Our network aims to connect public marijuana companies with these focused cannabis audiences across the US and Canada that are critical for growth: Short and long term cannabis investors Active funding sources Mainstream media Business leaders Cannabis consumers