Paysign Inc: Perfect Time to Make a Double, Fundamentals Surging

Marijuana Business, Stocks, Finance, & Investing August 10, 2020 MJ Shareholders 0

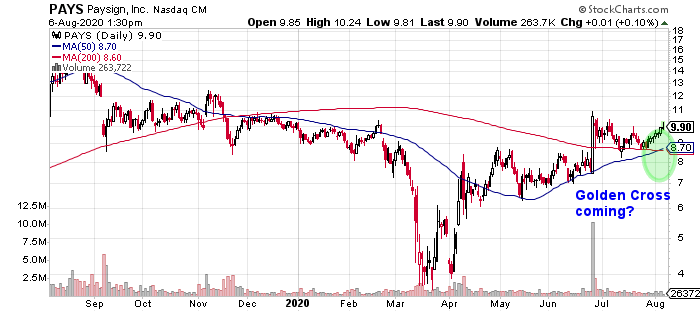

Paysign Stock Too Cheap to Ignore

After the massive 63% rally from the March lows, it’s difficult to find any technology stock that may have been overlooked, but I may have found one. Paysign Inc (NASDAQ:PAYS), a provider of payment solutions services, prepaid debit cards, rewards programs,and customizable payment services.

Paysign’s clients are found in sectors including healthcare, hospitality, pharmaceuticals, and retail.

PAYS stock plummeted to $3.63 during the March sell-off. It has rallied 178%, but Paysign stock remains well below its 52-week high of $17.46, down 26% over the past year.

PAYS stock could be set to signal a bullish golden cross pattern if the 50-day moving average can break above the 200-day moving average.

The chart shows that a breakout could send Paysign stock to $18.00.

Chart courtesy of StockCharts.com

Strong Fundamental Growth Supports Bullish Thesis for PAYS Stock

A glance at the company’s fundamentals supports why I feel Paysign stock is underappreciated and could be set for a significant rally.

Paysign Inc has recorded strong double-digit revenue growth in each of the last four years, to a record level in 2019. This implies an impressive compound annual growth rate (CAGR) of 43.8%.

| Fiscal Year | Revenues (Millions) | Growth |

| 2015 | $8.1 | |

| 2016 | $10.4 | 28.5% |

| 2017 | $15.2 | 46.3% |

| 2018 | $23.4 | 53.8% |

| 2019 | $34.7 | 48.0% |

(Source: “Paysign Inc.” MarketWatch, last accessed August 7, 2020.)

The forward estimates are optimistically strong, despite the COVID-19 threat.

Paysign Inc is expected to report revenue growth of 31% to $45.4 million this year and 40.9% to $64.0 million in 2021. (Source: “Paysign, Inc. (PAYS),” Yahoo! Finance, last accessed August 7, 2020.)

Paysign has also been reporting strong positive growth in earnings before interest, taxes, depreciation, and amortization (EBITDA), including setting a record in 2019.

| Fiscal Year | EBITDA | Growth |

| 2015 | $353,840 | |

| 2016 | $1.9 Million | 445.7% |

| 2017 | $2.6 Million | 36.9% |

| 2018 | $3.6 Million | 34.7% |

| 2019 | $7.6 Million | 112.9% |

(Source: MarketWatch, op. cit.)

The bottom line also looks impressive, with four consecutive years of growth in earnings per share (EPS), based on generally accepted accounting principles (GAAP).

| Fiscal Year | Diluted GAAP EPS | Growth |

| 2015 | -$0.06 | |

| 2016 | $0.03 | 150.0% |

| 2017 | $0.04 | 24.3% |

| 2018 | $0.05 | 32.4% |

| 2019 | $0.14 | 176.5% |

(Source: MarketWatch, op. cit.)

Looking ahead, Paysign Inc is estimated to report an adjusted $0.20 per diluted share this year, followed by $0.30 in 2021. (Source: Yahoo! Finance, op. cit.)

Paysign has been generating positive free cash flow (FCF), including four straight years of impressive growth.

| Fiscal Year | Free Cash Flow (Millions) | Growth |

| 2015 | -$1.6 | |

| 2016 | $1.2 | 172.9% |

| 2017 | $2.0 | 75.5% |

| 2018 | $4.2 | 106.6% |

| 2019 | $9.5 | 126.2% |

(Source: MarketWatch, op. cit.)

A look at the company’s balance sheet shows no debt, and $9.4 million in cash. (Source: Yahoo! Finance, op. cit.)

Analyst Take

In my view, it’s difficult to find a reason not to look at PAYS stock. There is some uncertainty, but the low share price discounts it, and Paysign stock could take off.

Insiders appear to be confident, and that’s a good sign. Over the last six months, insiders bought 700,000 Paysign shares and refrained from selling. (Source: Yahoo! Finance, op. cit.)

MJ Shareholders

MJShareholders.com is the largest dedicated financial network and leading corporate communications firm serving the legal cannabis industry. Our network aims to connect public marijuana companies with these focused cannabis audiences across the US and Canada that are critical for growth: Short and long term cannabis investors Active funding sources Mainstream media Business leaders Cannabis consumers

No comments so far.

Be first to leave comment below.