Medallia Stock: Time to Pounce on Underappreciated Digital Cloud Play?

Marijuana Business, Stocks, Finance, & Investing September 23, 2020 MJ Shareholders 0

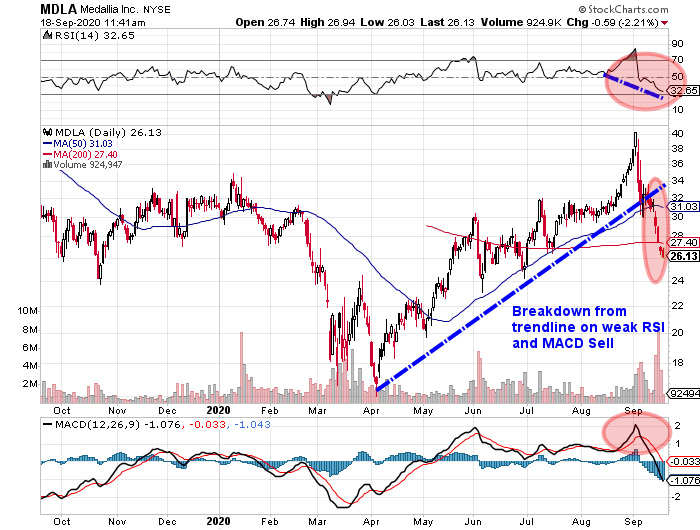

Medallia Stock at Attractive Entry Point; Down 34% from High

The tailwinds in the digital marketing space will be massive going forward as more companies look to maximize their digital revenue stream. A high-risk/reward cloud play that will benefit from the tailwinds is Medallia Inc (NASDAQ:MDLA).

After trading at a 52-week high of $40.20 on September 2, Medallia stock has retrenched 34% to attractive levels deserving of a look.

Medallia’s cloud platform enables companies to gain advanced insights into their customers in order to deliver a better experience and drive higher sales. Medallia deals with over 1,000 brands via over 15 offices worldwide.

The recent slide in Medallia stock was partly triggered by dilution concerns after the company announced a $500.0-million convertible note issue. But, while the concern is valid, I feel the company’s growth will compensate for the potentially extra shares of MDLA stock.

A look at the chart of Medallia stock shows the V-shaped rally and the subsequent uptrend supported by a strong relative strength index and moving average convergence/divergence.

MDLA has since broken down—breaking below its trendline to below its 50-day and 200-day moving averages. The next key supports are $26.00, $24.00, and $22.00.

Chart courtesy of StockCharts.com

On the upside, MDLA faces resistance at $32.00 to $34.00 and $40.00.

Pathway to Profitability Supports Bull Case

Medallia has generated strong revenue growth highlighted by double-digit growth in fiscal 2019 (ending January) and fiscal 2020.

But, at nearly 10 times trailing revenues, MDLA stock has a premium valuation.

| Fiscal Year | Revenue (Millions) | Growth |

| 2018 | $261.2 | N/A |

| 2019 | $313.6 | 20.10% |

| 2020 | $402.0 | 28.20% |

(Source: “Medallia, Inc.,” MarketWatch, last accessed September 18, 2020.)

The positive is that the revenue growth is expected to continue at 16.2% to $467.9 million in fiscal 2021, followed by $549.4 million in fiscal 2022, up 17.4% year-over-year. (Source: “Medallia, Inc. (MDLA),” Yahoo! Finance, last accessed September 18, 2020.)

If the numbers pan out, Medallia valuation would improve to 7.12 times fiscal 2022 revenues.

Medallia is reporting generally accepted accounting principles (GAAP) losses and negative earnings before interest, taxes, depreciation, and amortization (EBITDA), but the company is estimated to potentially deliver adjusted profits this year.

| Fiscal Year | GAAP Diluted EPS | Growth |

| 2018 | -$0.57 | N/A |

| 2019 | -$0.66 | -16.90% |

| 2020 | -$1.35 | -103.90% |

On an adjusted basis. MDLA could turn adjusted profits of $0.02 per diluted share in fiscal 2021 and then follow this with an adjusted $0.08 and as high as $0.12 per diluted share in fiscal 2022. (Source: Yahoo! Finance, op. cit.)

Medallia Inc is free cash flow (FCF) negative, but with revenues on the rise and potential profits around the corner, FCF could narrow and move towards positive territory.

In the meantime, MDLA carries $61.7 million in debt and ample cash of $347.5 million, enough to get through the pandemic without sacrificing growth.

Analyst Take

If you believe in the future of the digital space, Medallia stock would be an ideal play on this growth.

MDLA stock is not cheap based on old-school principles, but in the current valuations in technology, Medallia stock is not super-expensive, so it’s worth a look at the current level.

MJ Shareholders

MJShareholders.com is the largest dedicated financial network and leading corporate communications firm serving the legal cannabis industry. Our network aims to connect public marijuana companies with these focused cannabis audiences across the US and Canada that are critical for growth: Short and long term cannabis investors Active funding sources Mainstream media Business leaders Cannabis consumers

No comments so far.

Be first to leave comment below.