PagerDuty, Inc: Digital Cloud Stock on Verge of Breaking Out

Marijuana Business, Stocks, Finance, & Investing September 3, 2020 MJ Shareholders 0

PagerDuty, Inc: A Strong Revenue Grower

Strong tailwinds in the digital solutions segment will help power enterprise software providers like PagerDuty Inc (NYSE:PD).

The provider of cloud-based digital management solutions has tons of upside potential having largely missed out on the technology rally.

PD stock is up 29% this year, but remains around 50% below its record high in June 2019, where I see an aggressive buying opportunity.

Think about the demand for digital technology solutions as more companies work to strengthen their digital online presence.

This is where PagerDuty comes in, to help enterprise software developers with the operation of their digital presence.

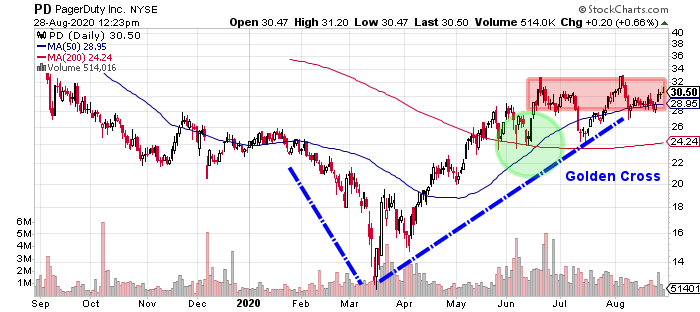

PagerDuty stock managed a strong V-shaped bounce from its March low of $12.33, which included the emergence of a bullish golden cross in June. This is a situation when the 50-day moving average breaks above the 200-day moving average, an indication of momentum.

Chart courtesy of StockCharts.com

The chart shows that PD stock is a tight sideways channel just above the 50-day moving average, looking for direction. A rally could drive PD to break $32.00, followed by key retracement levels at $35.00 and $40.00. The downside risk is $26.00 to $28.00.

Strong Revenue Growth Supports Bull Case for PD Stock

PagerDuty has only three years of reporting history after its initial public offering in June 2019.

But the revenue picture is impressive. PagerDuty ramped up revenues in 2019 (fiscal year ending January 31) and hit a record in 2020.

| Fiscal Year | Revenue (Millions) | Growth |

| 2018 | $79.6 | — |

| 2019 | $117.8 | 47.9% |

| 2020 | $166.4 | 41.2% |

(Source: “PagerDuty Inc,” MarketWatch, last accessed August 28, 2020.)

The forward growth looks to moderate to 25.2% to $208.3 million in 2021 and 22.0% growth to $254.0 million in 2022. This is not unexpected for growth companies like PagerDuty as they ramp up revenues. (Source: “PagerDuty Inc (PD),” Yahoo! Finance, last accessed August 28, 2020.)

PagerDuty has yet to turn a profit on both a generally accepted accounting principles (GAAP) and adjusted basis, but the losses are narrowing.

| Fiscal Year | GAAP Diluted EPS | Growth |

| 2018 | -$0.51 | — |

| 2019 | -$0.54 | -6.8% |

| 2020 | -$0.77 | -41.3% |

(Source: MarketWatch, op. cit.)

PD is estimated to narrow its adjusted loss to $0.27 per diluted share in 2021, compared to $0.35 per diluted share in 2021. And the positive trend is expected to continue as PagerDuty cuts its loss to $0.19 per diluted share in 2022 (Source: Yahoo! Finance, op. cit.)

Free cash flow is negative. Not a surprise, but the results have improved in two straight years.

| Fiscal Year | Free Cash Flow (Millions) | Growth |

| 2018 | -$12.6 | — |

| 2019 | -$9.7 | 23.2% |

| 2020 | -$5.4 | 45.0% |

(Source: MarketWatch, op. cit.)

Meanwhile, PD has strong working capital and minimal debt of $34.9 million, along with healthy cash of $350.8 million. During the current pandemic and its uncertainties, this will help PagerDuty. (Source: Yahoo! Finance, op. cit.)

Analyst Take

PagerDuty stock has seen a rise in buying from institutional investors. About 194 institutions hold a 71.51% stake in the outstanding shares of PD stock. (Source: Yahoo! Finance, op. cit.)

My bull case for PagerDuty stock is based on the strong revenue growth and the narrowing of the losses. At the current price, PD stock looks intriguing.

MJ Shareholders

MJShareholders.com is the largest dedicated financial network and leading corporate communications firm serving the legal cannabis industry. Our network aims to connect public marijuana companies with these focused cannabis audiences across the US and Canada that are critical for growth: Short and long term cannabis investors Active funding sources Mainstream media Business leaders Cannabis consumers

No comments so far.

Be first to leave comment below.