Why Smaller Psychedelics Companies Should Start Catching Up To The Sector Leaders

Marijuana Stocks, Finance, & InvestingUncategorized May 5, 2021 MJ Shareholders

- Five public companies totally dominate the psychedelic drug space, by market cap

- There are strong reasons to believe that such concentration is not sustainable

Wealth inequality has become a huge story in our societies. The reckless and unprecedented injections of capital into our markets and economies by central banks has (mysteriously) been concentrated as increasing wealth in the pockets of – relatively speaking – a handful of multi-billionaires.

However, market cap inequality among public companies is another huge story. Except it’s not called market cap inequality. It’s simply referred to as “concentration” of stock ownership. And in U.S. markets, it’s also at unprecedented extremes.

The general concentration of stock ownership in (specifically) U.S. markets is rather easily explained.

Fueled by the oceans of additional central bank funny-money, markets have largely degenerated into crazed casinos.

Manic gamblers, masquerading as investors, chase momentum. The fat get fatter while most other public companies drift.

This may make ‘sense’ (to the gamblers) with respect to the mature large caps that largely populate the S&P500 and even the NASDAQ.

These companies are generally in mature sectors. With multinational corporations totally dominating most of these sectors, increasing concentration of investor capital is at least somewhat understandable.

Psychedelic stock ownership becomes much more concentrated

What about the increasing concentration of ownership in psychedelic stocks?

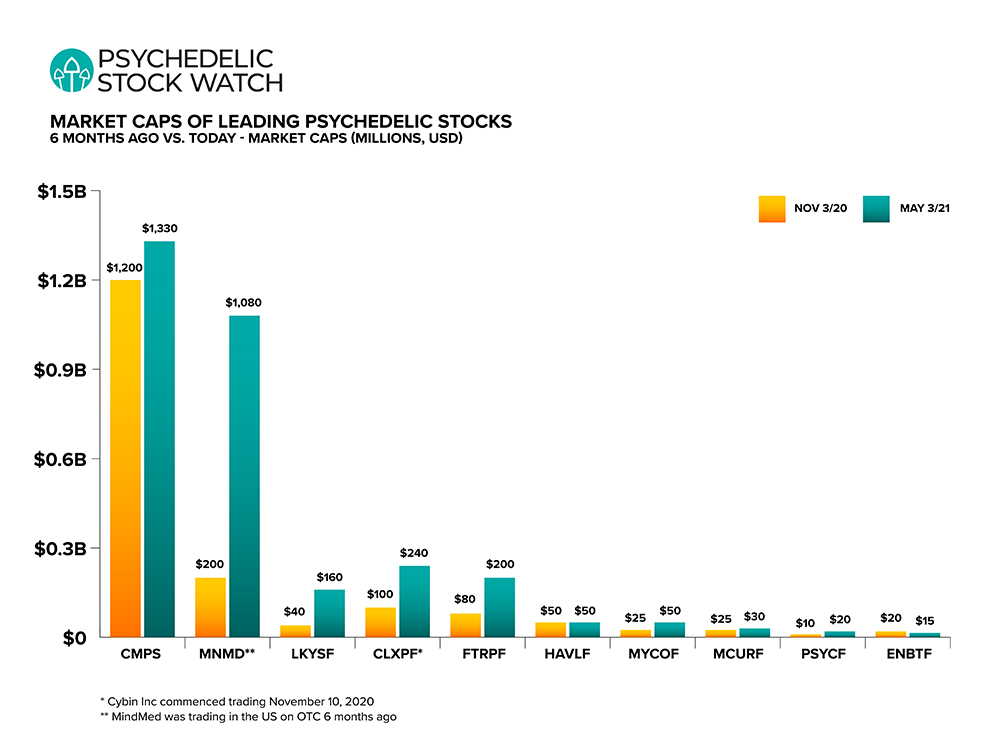

Immediately after the Compass Pathways (US:CMPS) IPO, there was one big fish in the sector: Compass Pathways itself. CMPS had a $1+ billion market cap.

The remainder of public companies were relatively evenly distributed in size: from microcap startups to a few companies in the $100 – $200 million range. Very little concentration outside of CMPS.

Concentration started during the big 2020 rally, which began when Compass commenced trading on September 18th. MindMed Inc (US:MNMD / CAN:MMED) and Numinus Wellness (CAN:NUMI / US:LKYSF), in particular, began to outpace other stocks by a wide margin.

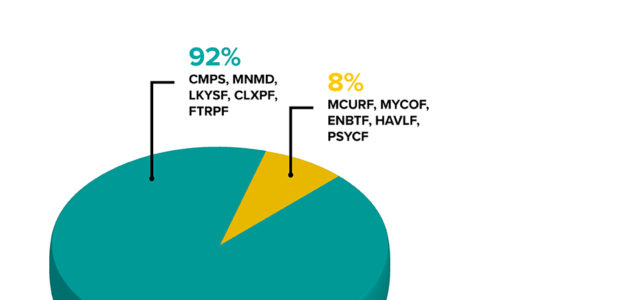

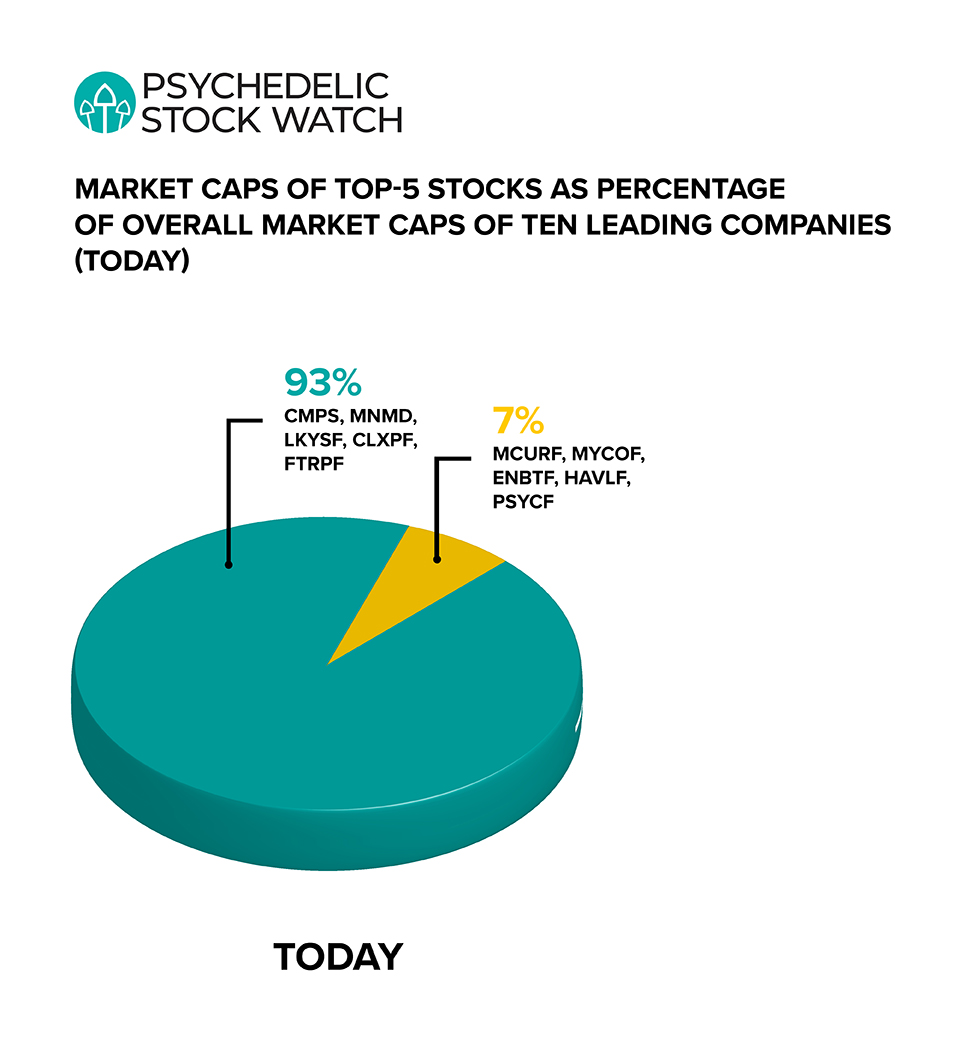

By early November, concentration in the top-5 stocks was near its 2020 peak.

Again, this is somewhat understandable. In any significant market rally, an investor’s portfolio tends to become more concentrated as the winners outpace the also-rans.

However, market cap concentration among psychedelic stocks has continued to increase and is actually higher today. This comes with most stocks well off previous highs and overall conditions in the sector not as hot as they were last fall.

This concentration parallels behavior in the broader markets. But does it make any sense in a rapidly emerging sector like the psychedelic drug industry, powered by massive capital infusions?

And these capital flows have been filtering down to even the smaller players in the industry.

The largest players in the sector, notably Compass and MindMed, have raised roughly 10 – 15 times as much capital as many of the intermediate companies in this space. But their market caps are 20X to 30X greater – with ratios even more skewed versus a couple of these other companies.

Part of this disparity can be explained by the influx in new public companies. Retail investor capital among the smaller players has become somewhat diluted, as those dollars are spread across a lot more companies.

The net result is that the market caps of five companies now totally dominate this sector. And this does not appear to make sense – given the impressive dynamics of the psychedelic drug industry.

A huge opportunity, increasing exponentially in size

It was clear when investors first began gravitating to psychedelic stocks that there was a big investment opportunity on the table here.

The Mental Health Crisis.

- 1+ billion potential consumers of psychedelic drugs

- Game-changing results in clinical trials of psychedelic drugs

- Wide open treatment markets due to the current abysmal standard of care

But this opportunity keeps getting bigger and bigger and bigger.

The Mental Health Crisis is not just worsening. It is spiraling out of control at an exponential rate.

Already, as many as 1 in 4 people across the planet are now suffering from some form of mental health disorder, brought on by the numerous severe stresses associated with COVID-19 lockdowns.

Meanwhile, psychedelic drug R&D is branching out into other fields of medical treatment at an equally rapid pace. And this research is targeting many of the world’s largest medical treatment markets.

The investment opportunity in psychedelic drugs is expanding exponentially both vertically and horizontally.

Is there room in this space for only five winners?

It’s not a question that is even worthy of an answer – not in a sector still in its infancy that has seen over US$700 million of investment capital flood into the industry, in roughly just the last 6 months.

There is more than enough capital entering this sector to drive the stocks of a lot more than five public companies. And yet today we’re seeing only five winners.

Psychedelic Stock Watch has already pointed toward one investment window where we may start to see this market cap disparity recede.

Will atai’s IPO lead to greater market cap equality?

Atai Life Sciences has now filed for its IPO financing. A trading date on the NASDAQ could be announced at any time.

It’s easily the most-anticipated psychedelics IPO, as atai is immediately expected to become the new industry leader among public companies. That would broaden the concentration from five to six stocks.

But it doesn’t really alter the concentration equation. Atai is already a (private) behemoth in this industry.

Given the fever that surrounds highly anticipated IPOs these days, it is very likely that many would-be investors in atai will experience sticker shock on IPO day, and not be willing to buy into atai at such an inflated market cap.

Where will those extra dollars go?

Yes, companies like Compass and MindMed and Cybin all have ongoing Phase II clinical trials. But so does Mydecine Innovations Group (CAN:MYCO / US:MYCO) – and it’s market cap is a compact CAD$64 million (~US$50 million).

Yes, Field Trip and Numinus are developing robust networks of mental health clinic services. But Novamind Inc (CAN:NM / US:NVMDF) has clinic operations of a comparable scale to the two larger companies. Its current market cap is only CAD$56 million (~US$45 million).

Private company, Mindstrong, closed a US$100 million financing in 2020. Its operations are solely focused on its AI-powered digital therapeutics platform.

Mind Cure Health (CAN:MCUR / US:MCURF) is building out its own AI-powered digital therapeutics platform and already has a mental health treatment site in place to deploy that platform as it seeks to commercialize this IP. MCUR is also active in drug development and nootropics manufacturing/distribution. But it’s market cap is only CAD$38 million (US$30 million).

These are not fly-by-night companies. They are well-capitalized smaller players in the industry. With any significant operational breakthrough, they could quickly/easily start closing the market cap gap with the larger companies.

And they are not alone.

Several other psychedelics pubcos offer (at least) interesting investment possibilities. One major announcement, or even one major institutional investor coming onboard, and some of these other stocks could take off as well.

Best value opportunities in the smaller companies

Originally, “concentration” in psychedelic drug stocks was one company: Compass Pathways.

Then two more leaders emerged: MindMed and Numinus. And then two more after that (Cybin and Field Trip). But for the past 6 months the industry has remained frozen, in terms of concentration.

The massive capital flows alone dictate that more public companies should be joining this winners’ circle.

As noted, atai doesn’t alter this dynamic, since it was always assumed the company was going public. And atai has been the best-capitalized company (public or private) since Day 1 of this industry.

When will some of these smaller, dynamic players in the psychedelic drug industry start outperforming their larger peers?

It should have already happened. In terms of both the capital raised by these companies and their own progress on operations, they merit more competitive market caps versus the largest pubcos.

More pertinently, if (when?) it does happen, the upside potential of these smaller companies dwarfs the larger pubcos.

We need look no further than Compass and MindMed.

Compass Pathways immediately had a market cap in excess of $1 billion. At that time, MindMed’s market cap was under US$100 million.

Today, the market caps are roughly equivalent. In other words, MindMed has outperformed CMPS by greater than a 10:1 margin.

Obviously, those who bought into MindMed at/before the CMPS IPO have done very well for themselves.

With MindMed’s deep drug development pipeline, this is a rather extreme example. But as noted, some of these other developing companies also offer some exciting investment prospects – prospects which are currently not being recognized (and priced in) by the market.

Early MindMed investors have already reaped a ten-bagger in their psychedelics investments.

But it’s much less likely that MindMed will duplicate that performance going forward (i.e. generate a 100X return).

Those investors will now be looking elsewhere for their next 10X return in psychedelic stocks. Where will you look for the next psychedelics ten-bagger?

DISCLOSURE: The writer holds shares in MindMed Inc, Numinus Wellness, Cybin Inc, Mind Cure Health and Novamind Inc.

MJ Shareholders

MJShareholders.com is the largest dedicated financial network and leading corporate communications firm serving the legal cannabis industry. Our network aims to connect public marijuana companies with these focused cannabis audiences across the US and Canada that are critical for growth: Short and long term cannabis investors Active funding sources Mainstream media Business leaders Cannabis consumers