The Importance of Cannabis Debt Scoring During the Capital Crunch

FeaturedTrending Stories January 20, 2020 MJ Shareholders 0

Guest Post by Frank Colombo, Partner and Chief Risk Officer of Aspen Finance LLC

The cannabis debt wave is coming!

Despite solid efforts to reduce cash burn, cannabis companies will require significant amounts of financing in 2020 to complete their build-outs and strategic acquisitions but…

The equity market is virtually closed to a large swath of cannabis companies. Even those with solid business positions and clear paths to profitability will find selling equity painful at the new price levels. Expect to see a marked increase in distressed asset sales from companies who probably could have sold equity in early 2019.

The cannabis crash of 2019 occurred because the growth and margin assumptions required to support earlier valuations were too extreme. Investor expectations regarding growth rates, time to cash positive, stabilized EBITDA margins, costs of capital, and the difficulty of eliminating the illegal market, have been adjusted, and cannabis equities are now more fairly priced. The market may recover a bit from here; however, barring a major catalyst like full federal legalization (which doesn’t seem likely in the near term), those heady IPO/RTO prices are gone for good.

There is lots of room for debt in the cannabis capital structures. Debt, including equity-linked debt, like convertibles, accounts for only 12.9% of market capitalization for the top 25 U.S. public cannabis companies:

- Most banks and financial institutions are unable to lend to cannabis companies, and this is unlikely to change in 2020. Private capital is increasingly stepping in to fill the void, driven by the extremely attractive returns.

- Historically this nascent industry presented too high a risk for fixed rate investors. Accordingly…

- Most cannabis debt has been convertible with low conversion premiums – essentially representing delayed equity issuance. Many deals have paired convertible debt with detachable warrants for combined coverages of well over 100%. The “stripped yields” (yields with conversion features removed) on these converts are eye-popping and the few straight coupon deals have been equally attractive.

The credit quality of the industry is now at a tipping point. 18 out of 25 U.S. cannabis companies profiled are expected to be EBITDA positive in 2020 (versus 8/25 in 2019), supporting the inclusion of debt in their capital structures. Debt capacity (calculated at 3 times consensus estimates of 2020 EBITDA) is approximately $4 billion compared to outstanding debt of about $1.8 billion ($0.5 billion of which is MedMen alone!).

The trend towards straight debt issuance has begun with the recently announced $275 million 13% term loan from Curaleaf and the $73 million 15% senior secured notes from Harvest Health and Rec. But make no mistake – only the top tier of credits will be able to issue debt without warrants. Pricing for mid-tier credits will likely improve with lower warrant coverages and higher exercise premiums. Meanwhile, in the midst of this new debt issuance wave, 2020 will be the real kickoff for cannabis distressed debt trading, complicated by the unavailability of Chapter 11.

Don’t look for any help from the rating agencies in your investment decision

Neither S&P nor Moody’s has issued any credit rating in the cannabis market and neither seems to be in any rush to jump in. It will probably take a minimum of the SAFE Banking Act before the agencies get involved.

The accounting can be byzantine, trusted ratios may fail, and neither the companies nor most managements have much operating history.

Many U.S. investors, who are not familiar with IFRS accounting, will struggle with the dramatic and volatile impacts that IFRS mark-to-market adjustments can have on gross margins and inventory valuation. Tried-and-true credit ratios like EBITDA/Interest and Debt/EBITDA may be relatively meaningless when the companies have negative EBITDA and very little debt. In addition, few of these companies have more than 2 years of operating history.

Discerning relative credit quality through the smoke

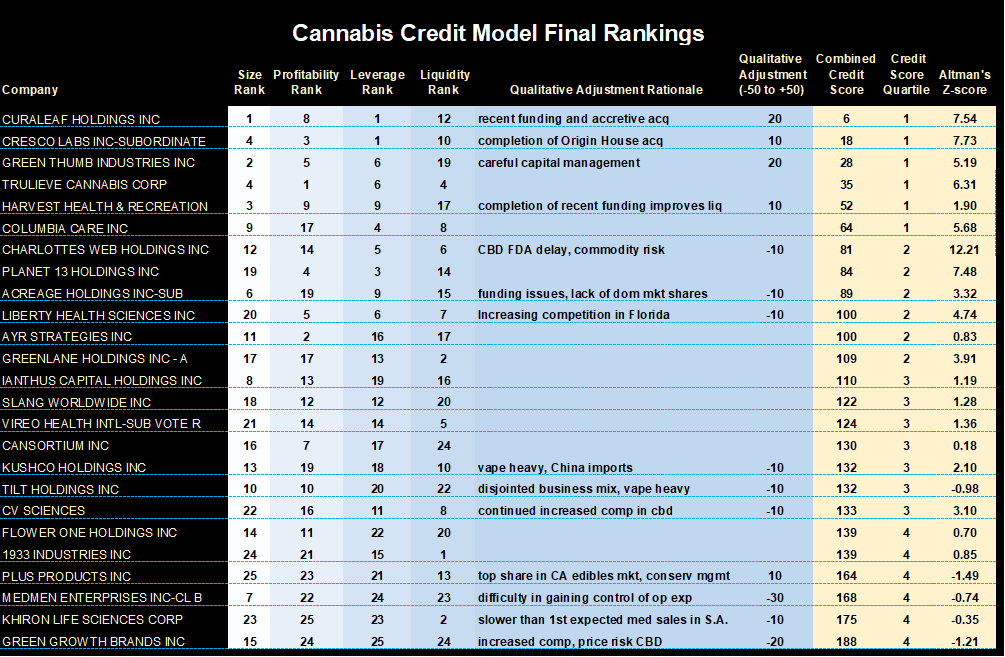

A simple yet robust credit ranking model will be a prized tool for portfolio managers first dipping their toes in the cannabis debt market. I have developed an effective model that is customizable and incorporates data from financial statements and market pricing as well as optional user inputs on qualitative factors like management quality, regulatory environments, business sector risk, and competition.

The model produces the following ranking of the top 25 public U.S. cannabis companies utilizing Q3:2019 financials and 1/16/20 equity prices:

About the author:

Frank Colombo is Partner and Chief Risk Officer of Aspen Finance LLC, a fund established to lend to and invest in the cannabis industry. Frank is a seasoned executive with over 20 years of success in consulting, credit research, valuation, and financial planning and analysis. He was formerly Global Head of High Yield Research at UBS and Managing Director/Head of Research at Seaport Group LLC.

He holds a BA summa cum laude from University of Colorado, an MBA from Stanford University, and a CFA.

Frank is available for strategy, financial analysis and valuation consulting and can be reached by emailing fcolombocfa@gmail.com.

Get ahead of the crowd by signing up for 420 Investor, the largest & most comprehensive premium subscription service for cannabis traders and investors since 2013.

Get ahead of the crowd by signing up for 420 Investor, the largest & most comprehensive premium subscription service for cannabis traders and investors since 2013.

MJ Shareholders

MJShareholders.com is the largest dedicated financial network and leading corporate communications firm serving the legal cannabis industry. Our network aims to connect public marijuana companies with these focused cannabis audiences across the US and Canada that are critical for growth: Short and long term cannabis investors Active funding sources Mainstream media Business leaders Cannabis consumers

No comments so far.

Be first to leave comment below.