Switch, Inc: Data Center Play Up 76% This Year But Can Double From Here

Marijuana Business, Stocks, Finance, & Investing June 7, 2019 MJ Shareholders 0

Switch Inc Set to Benefit From Huge Data Centers

While cloud storage has become integral for many companies to store data, there is also increasing demand from companies to store their physical IT assets in what is known as colocation data centers.

The thinking is that storing technology assets at a third-party location helps to reduce the need to spend on expensive in-house facilities and reduce the threat of storing all assets in-house in case something disastrous happens.

A mid-cap player in the data center market with above average upside is Switch Inc (NYSE:SWCH), which is outperforming with a 76% gain this year but underperforming over the last year, down six percent.

With SWCH stock trading 28% below its initial public offering (IPO) price of $17.00 in October 2017, there is an opportunity to accumulate shares.

Switch is presently running three advanced primary colocation data locations with a capacity of up to four-million gross square feet of space. A fourth center is planned.

The company’s client list is broad, including technology, digital media, cloud and managed services, financial institutions, and telecommunications companies.

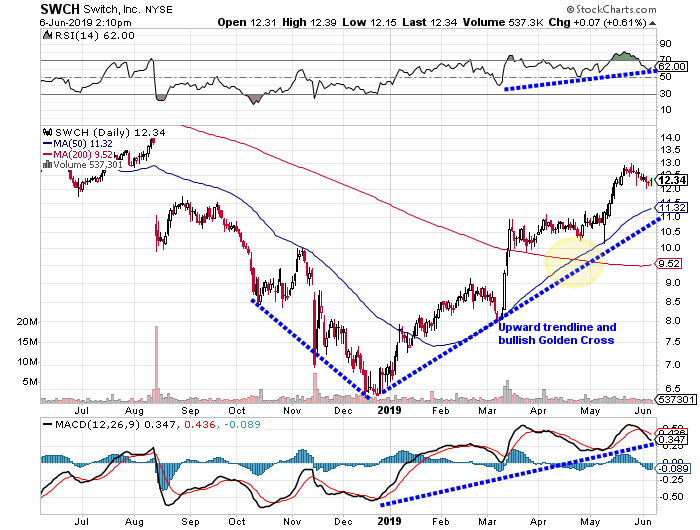

The Switch stock chart displays the downside break in August 2018 to the December low prior to the V-shaped rally:

Chart courtesy of StockCharts.com

Watch for strong support at around $8.00 to $9.00 for SWCH stock. If the momentum returns to the technology sector and Switch can deliver, there is no reason why SWCH stock cannot trade back at its IPO price.

My Bullish Case for SWCH Stock

Revenues have increased in three consecutive years, starting with $265.87 million in 2015 and going to to $405.86 million in 2018.

| Fiscal Year | Revenue ($Millions) | Growth |

| 2015 | $265.87 | – |

| 2016 | $318.35 | 19.7% |

| 2017 | $378.28 | 18.8% |

| 2018 | $405.86 | 7.3% |

(Source: “Switch, Inc.,” MarketWatch, last accessed June 6, 2019.)

The decline in the revenue growth rate was disappointing, but Switch Inc is estimated to turn things around with growth of nine percent to $442.48 million in 2019 and as high $510.99 million in 2020. (Source: “Switch, Inc. (SWCH),”Yahoo! Finance, last accessed June 6, 2019.)

How fast revenues grow will depend on adding capacity and clients.

That said, Switch is producing positive earnings before interest, taxes, depreciation, and amortization (EBITDA), including strong growth of 48.57% to $161.35 million in 2018.

| Fiscal Year | EBITDA ($Millions) | Growth |

| 2015 | $134.91 | – |

| 2016 | $144.68 | 7.2% |

| 2017 | $108.60 | -24.9% |

| 2018 | $161.35 | 48.6% |

(Source: MarketWatch, op. cit.)

Switch is also profitable, but needs to deliver steady growth.

| Fiscal Year | Diluted EPS | Growth |

| 2015 | $2.04 | – |

| 2016 | $0.87 | -57.3% |

| 2017 | -$1.88 | -315.4% |

| 2018 | $0.09 | 104.7% |

(Source: Ibid.)

Earnings are expected to double to $0.18 per diluted share in 2019 and go as high as $0.31 per diluted share in 2020. (Source: Yahoo! Finance, op. cit.)

The company has yet to generate positive free cash flow (FCF), but should be moving towards that as profits ramp higher.

Analyst Take

Switch has decent support from institutional investors. About 138 institutions hold 61.41% of the outstanding shares. (Source: Ibid.)

Valuation is not important at this time as long as Switch Inc ramps up revenues and moves towards delivering steady earnings growth and positive FCF.

MJ Shareholders

MJShareholders.com is the largest dedicated financial network and leading corporate communications firm serving the legal cannabis industry. Our network aims to connect public marijuana companies with these focused cannabis audiences across the US and Canada that are critical for growth: Short and long term cannabis investors Active funding sources Mainstream media Business leaders Cannabis consumers

No comments so far.

Be first to leave comment below.