December 2019 – Hemp Market Update

CBDHempMarijuana Industry News December 31, 2019 MJ Shareholders 0

Spot Market Updates

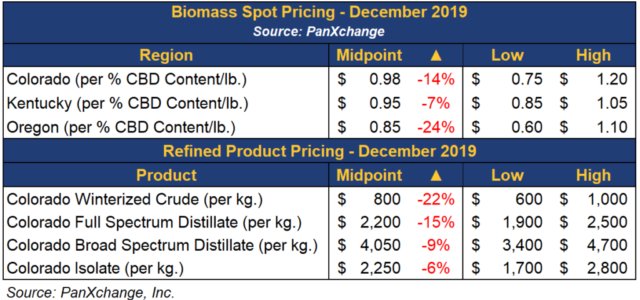

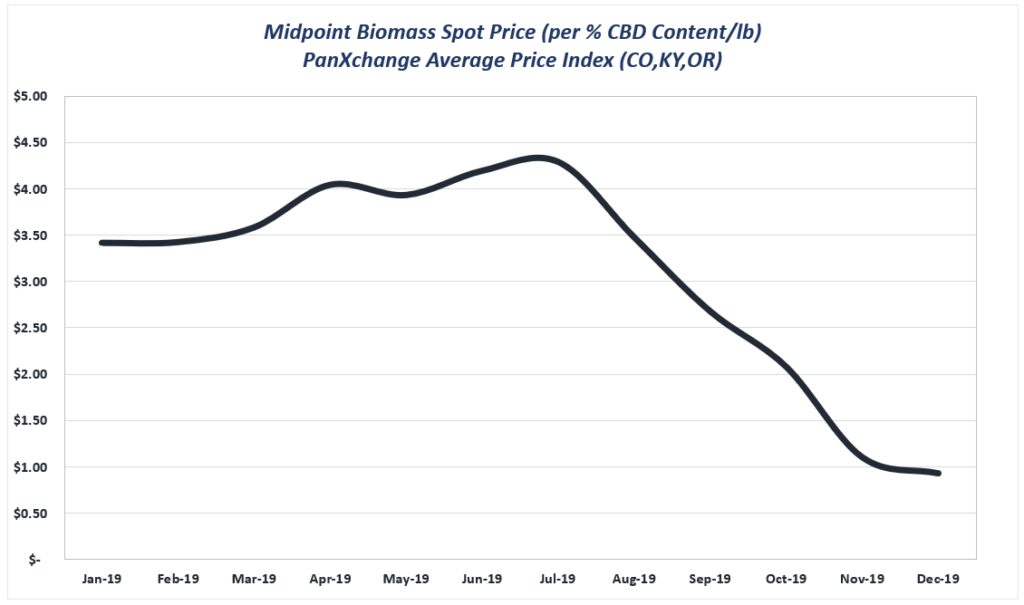

Biomass markets continue to bifurcate between two markets: 1) the market transacting at fair market values dictated by supply and demand; 2) a market rife with desperate sellers and opportunist buyers. Because of this fragmentation, recent transaction prices vary widely. In general, homogenized biomass prices have continued to soften, with prices across the country firmly at or below $1 per percentage point of CBD. Nontheless, the bid/ask spread has narrow since last month as product has been forced to move and buyers and sellers found common ground.

Unlike more mature commodity markets, behavior in the hemp market remains erratic, wherein a subtle gap in quality fragments the market even further. Biomass and smokable flower are particularly vulnerable. Specifically, one undesirable variation in biomass or a smokable flower which doesn’t have an optimal “nose” is the difference between a product that can be sold for consumption and one that is unusable and will go to waste. Quality concerns remain a pertinent topic, especially with biomass as industry participants are becoming more concerned with contaminants such as mold and heavy metals, as well as the impending USDA rules that were released a month ago.

CBG biomass continues to garner interest in the market, with offers posted on PanXchange’s trading platform between $150/lb and $200/lb for near term delivery.

Refined Product Pricing:

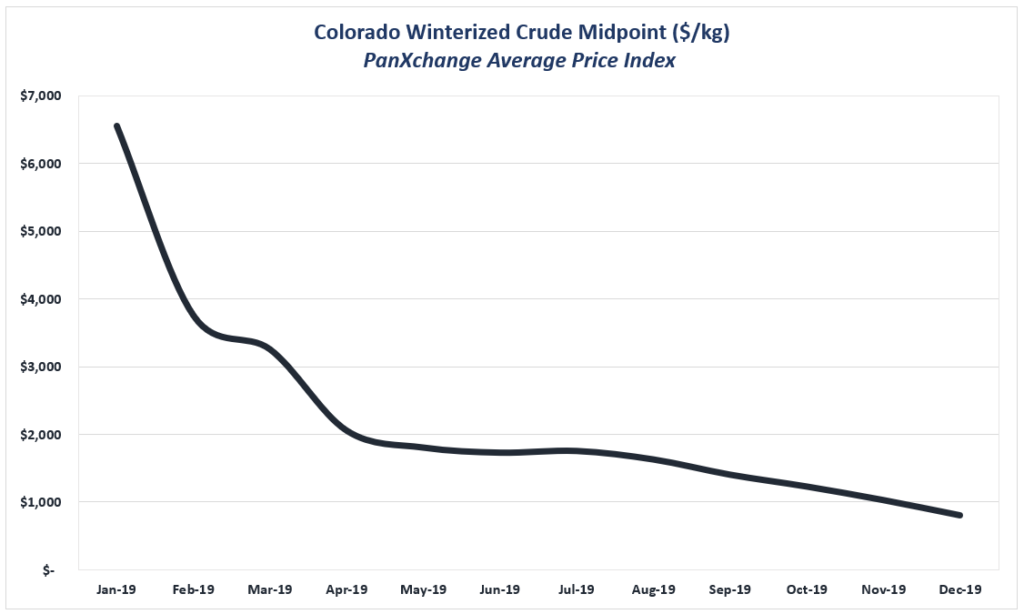

Market movement for winterized and non-winterized crude is extremely slow, which is an effect of the tolling splits, as discussed in previous PanXchange reports. Farmers who are removed from the refined product ecosystem, are now in possession of crude oil, often without the network or resources to locate buyers. Therefore, these farmers are willing to let the crude go for pennies on the dollar, driving prices down for the entire market in this product category.

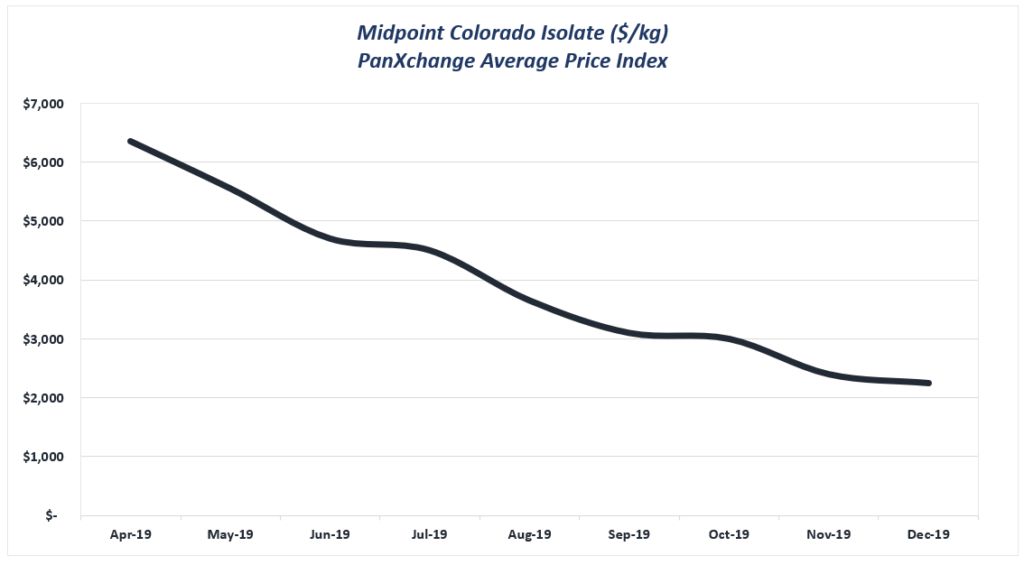

Distillate prices have continued to soften, with about a 15% decrease from last month’s index price, both in broad spectrum and full spectrum. Broad spectrum offers range from $2800/kg to $4700/kg. Full spectrum is trading at a significant discount to broad spectrum, with the major cost difference the THC remediation process. Full spectrum distillate is offered between $1900/kg and $2500/kg.

Isolate movement continues to be slow, with many producers switching their formulations to distillate due to concerns of pending patent exclusivity. Isolate has been offered on the PanXchange trading platform as low as $1800/kg, which is dangerously undervalued, and at that price point, it is difficult for any producer to generate a profit.

In summary, until we get a clear picture of true supply, demand, and processing capabilities, one cannot anticipate future price movements in this nascent market. Moreover, there are substantial price gaps based on quality. Finally, as you will see below, since hemp is presently a buyer’s market, so they may cherry pick their supply based on very specific quality and effectively apply pressure on pricing.

Industrial Hemp Demand

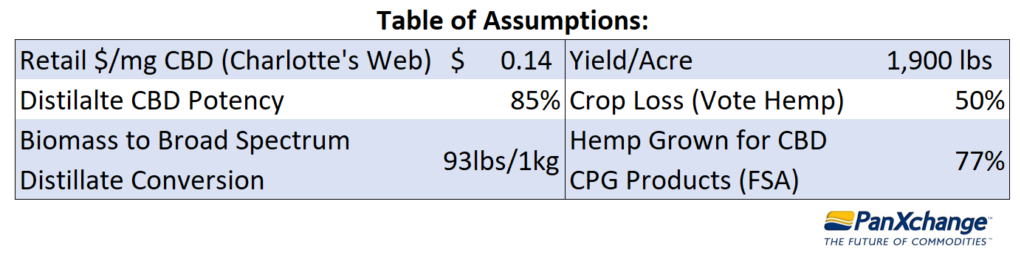

Note that each of the three scenarios below are based on the following assumptions:

Scenario 1: Charlotte’s Web: A case study

Charlotte’s Web is one of the largest hemp consumer packaged good (CPG) manufacturers, and one of the few that are publicly traded. As such, we used their financial statements as a case study to assess demand.

According to their third quarter statement, Charlotte’s Web projected between $90 million and $100 million in revenue for the calendar year 2019.

Taking $95 million in revenues from the sale of CBD products, and averaging the $/mg sales price from all individual products on the website ($0.1439/mg), we deduced the amount of refined product (distillate) accordingly. Assuming distillate with an 85% CBD potency, Charlotte’s Web needed approximately 776 kilograms of distillate to fuel its supply chain in 2019. Thus, Charlotte’s Web would achieve its stated revenue target with approximately 460 acres of hemp grown in 2018 for the 2019 marketing year. In the 2019 growing season, Charlotte’s Web increased hemp acreage to 862 acres, giving them a significant runway to increase sales in 2020 or carry a surplus into 2021. Note that the report claims that they do not sell raw material— biomass and refined inputs into the market in the event of a surplus.

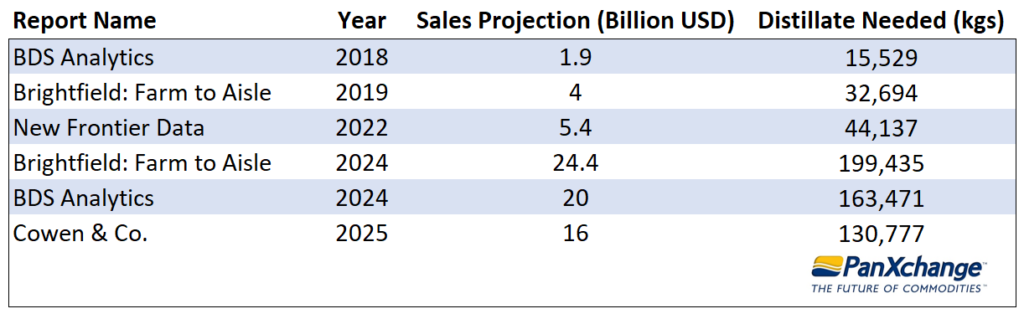

In conclusion, one of the largest US CBD brands needed less than 800 kg of finished product and less than 500 acres of hemp to service sales at an estimated $95 million in 2019. Taking the Brightfield estimate of total CBD sales in the United States of approximately $4 billion (see below), Charlotte’s Web would comprise 2.4% of sales. If we assume a uniform efficiency in hemp growth to consumer packaged good production, the United States hemp market would need just shy of 20,000 acres.

Scenario 2: Brightfield Group: Market estimates for consumer packaged goods (CPG)

Of the three scenarios described in this report, this is by far the most popular forecasting method. However, at PanXchange, we find it to be misleading. It is the job of the commodity merchandiser to assess current and future prices, relying on current and historical hard figures of actual physical supply and demand. In the absence of that, even the USDA is temporarily using market values to assess total sales for hemp farmers.

Unfortunately, we have not even been able to ascertain the supply and market prices these analysts used to reach these forecasts. These projections incentivized so many to jump into the hemp market this year and compete for their share. The reality is that these estimates are based on the retail shelf price of consumer packaged goods that contain mere milligrams of actual hemp product. We know that this market will continue to grow at a rapid pace, but for the moment, we are grossly oversupplied with raw hemp ingredients as shown below.

Note that we applaud analysts like Brightfield Group, who are attempting to bring clarity to the topic. We chose them to take a deep dive as they are the only analysts we found who published a 2019 forecast (see chart below). We do not intend to disparage their and others’ efforts to keep honing forecasts as hard data becomes available.

The Brightfield Group’s Farm to Aisle: 2019 CBD Market Report, assessed 2019 CBD sales at $4 billion. Using 14.39 cents/mg CBD from the previous example, the industry would need just shy of 32,000 kg of distillate to service the entire US market (assuming no loss of cannabinoids during product formulation). Projecting this out to the same projection of $24.4 billion in 2025 (which is one of the most aggressive projections), the US market would be supplied by just shy of 200,000 kg of 85% distillate.

Scenario 3: Demand estimate based on population data

Our third and final look at demand uses the US population estimate at 329 million. Assuming that 10% of the US population consumed CBD at a rate of 30mg/day, the US would consume 423,906 kilograms of 85% potency distillate a year.

Processing capacity is still a great unknown, and given that there are over nine different variables that affect the conversion from biomass to distillate, we’d be remiss to declare an average conversion. However, it’s important to begin the discussion on the biomass to distillate conversion so that we can begin to tie actual supply with demand. Therefore, based on conversations with industry processors, we’re going to use a baseline that it takes 93 pounds of 10 percent CBD biomass to yield one kilogram of THC remediated broad spectrum distillate. In this scenario, the CBD industry would need about 40 million pounds of biomass, which can be grown on approximately 20,700 acres taking into account yield of 1,900 pounds of homogenized biomass per acre planted, ready for extraction.

Globally, New Frontier Data, in New Year’s Worth of Pressing Topics for the Hemp Industry, assessed the US market to be 28% of global sales of CBD consumer packaged goods . As such, global demand for CBD distillate would be at 1,513,950 kg, yet the increase in demand globally is likely to be covered by other suppliers around the globe.

2019/2020 Supply

Vote Hemp’s estimate for 2019 hemp production at 230,000 acres planted and a 50% crop loss, yields a total of 115,000 acres. Moreover, 77% of hemp was planted with the purpose of CBD extraction (addressed in previous PanXchange reports and derived from the Farm Services Agency Crop Acreage Report), resulting in an estimated US production of 168,245,000 pounds of biomass throughout the 2019 harvest. If all biomass was converted to distillate, this would total 2.3 million kg (see the table of assumptions for conversion rates). We know that the US current processing capacity is not that large and not every pound will be harvested and converted into distillate. Nonetheless, it illustrates the enormity of the market’s total oversupply.

Conclusions

We need to emphasize that we, nor seemingly any entity in the industrial hemp market, is in a position to treat the analysis in this report as verified facts. However, we feel it’s important to let the industry know that with a few of the assumptions used herein, and looking at this market from three different angles, PanXchange believes that the current oversupply is significantly more than many in this market assume. As shown with Charlotte’s Web, one of the largest CBD product manufacturers need only an estimated 500 acres or 800 kg of distillate to reach $95 million in revenue. In our second scenario using Brightfield’s $4 billion of 2019 CBD sales, we project that the market would be satisfied with 32,600 kg of distillate. Taking the longer view, the same report has projected sales of CBD products to exceed $24 billion in 2025. If the same math was used, the 2025 market would be supplied on just shy of 200,000 kg of distillate, which would still be covered by the 2018 harvest. Note that these numbers do not account for smokable hemp or any non-CBD industrial purposes.

Yet it’s no wonder so many ventures are launching in the CBD space. One consumer taking 30 mg per day would spend over $600/year if the CBD cost is $0.05 mg and spend over $1,500/yr if the cost were $0.1439 mg (see section 1). Therein lies the hidden discrepancy of today’s market. If the average CBD consumer packaged goods (CPG) has 500mg of CBD , that same 85% distillate kilogram will yield 1,700 units.

As part of normal market maturation, input prices and retail prices will continue to drop, and volume will increase. Of course, a positive FDA ruling, including a statement that cannabinoids will be recognized as Generally Regarded as Safe (GRAS), will help boost demand. Over time, even though the CBD sales will continue to grow, it is only one sector when looking at the potential uses of the hemp plant. Falling prices due to oversupply are not only normal in market maturation but necessary. Seed costs have fallen 66% to approximately $1.00/seed ($3.00/seed one year ago). This decline in input prices, coupled with improvements in harvesting and processing, will drive production costs down, which will keep the CBD consumer packaged goods market afloat as retail prices continue to drop due to competition. Moreover, lowered input costs and processing efficiencies will galvanize demand for industrial hemp products such as cotton for textiles, petrochemicals for plastics, corn for biofuels and feed.

______________________________________________________________________________

A Note from PanXchange’s CEO:

Dear PanXchange community,

How quickly a year goes by!

I want to thank everyone in our community for your trust and support since we burst into the hemp scene a year ago. PanXchange was the first to market with benchmark prices in January, and we launched the industry’s only institutional grade trading platform in August. Today, we are the country’s leading provider of both trading and benchmark pricing. This wouldn’t have been possible without the hard work of our entire team and I’m very proud of their dedication, long hours, persistence and results.

As a former commodity trader with Cargill and other firms, I’ve been deeply frustrated at the lack of hard data. How can one accurately predict market size, prices, and forward curves without this baseline? Sure, we had to begin this year by using the number of acres licensed as a starting point for supply, but there have been no attempts- until now- to give predictions on actual demand. We’re going big this month by attempting to put the industry’s first estimates of the 2019 supply and demand outlook in terms of actual quantities, not predicted market values. What’s most concerning is that, because they’re the only numbers out there, the industry at large is hanging onto a handful of analysts’ predictions for the growth of the CBD in terms of total market value. These estimates are based on retail shelf prices of consumer packaged goods products that contain mere milligrams of hemp-derived products. It’s the tail wagging the dog (see Scenario 2) and although we are extremely bullish on industrial hemp as a viable agricultural sector in the US long term, we feel that the actual demand in 2019 for hemp for CBD products is dramatically less than most people had expected.

In this month’s article, we look at demand from three different angles. It’s not all encompassing, and while it’s based on the best data that is publicly available, unfortunately, it still relies on a significant amount of assumptions as you see below. We hope this begins a productive, industry-wide dialogue on supply and demand by deal flow, not market values based on wholesale and retail projected sales values.

Wishing you all a very joyful holiday season,

Julie Lerner

MJ Shareholders

MJShareholders.com is the largest dedicated financial network and leading corporate communications firm serving the legal cannabis industry. Our network aims to connect public marijuana companies with these focused cannabis audiences across the US and Canada that are critical for growth: Short and long term cannabis investors Active funding sources Mainstream media Business leaders Cannabis consumers

No comments so far.

Be first to leave comment below.