Glass House Q1 Revenue Pulls Back 10% From Q4

FeaturedTrending Stories May 16, 2023 MJ Shareholders 0

Glass House Brands Reports First Quarter 2023 Financial Results

- Achieved Positive Free Cash Flow1

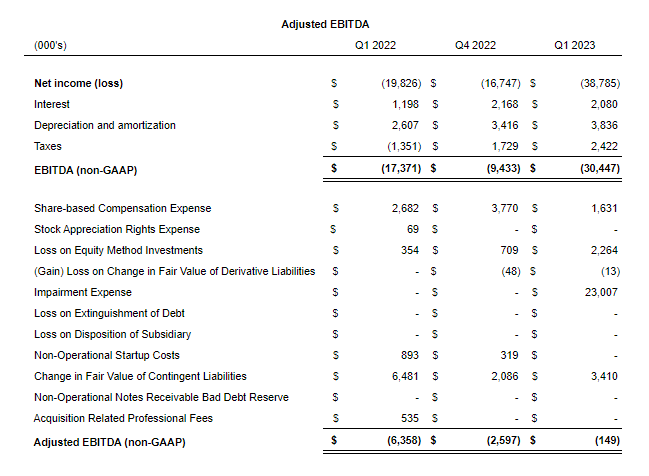

- Narrowed Adjusted EBITDA2 loss to $0.1 million versus $2.6 million loss in Q4

- Revenue of $29.0M, up 108% from Q1 2022

- Gross margin of 41% versus 32% in Q4 2022 and 17% in the prior year period

- Q1 Biomass production3 up 188% year-on-year and biomass revenue increased 182% year-on-year

- Cost of production of $196 per pound3,4, down 18% versus Q1 2022

- ASP $290 per pound, up 54% versus last year and 23% versus Q4

- Expect to have positive operating cashflow and positive adjusted EBITDA in Q2 and for the rest of the year

- Conference Call to be Held May 15, 2023 at 5:00 p.m. ET

LONG BEACH, CA and TORONTO, May 15, 2023 /CNW/ – Glass House Brands Inc. (“Glass House” or the “Company”) (NEO: GLAS.A.U) (NEO: GLAS.WT.U) (OTCQX: GLASF) (OTCQX: GHBWF), one of the fastest-growing, vertically integrated cannabis companies in the U.S., today reported financial results for its first quarter ending March 31, 2023.

First Quarter 2023 Highlights

(Unless otherwise stated, all results and dollar references are in U.S. dollars)

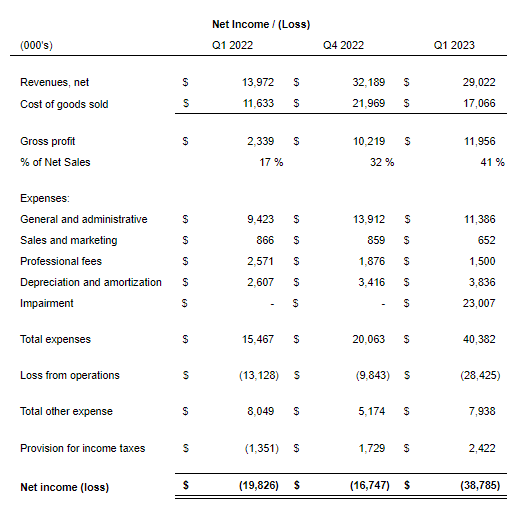

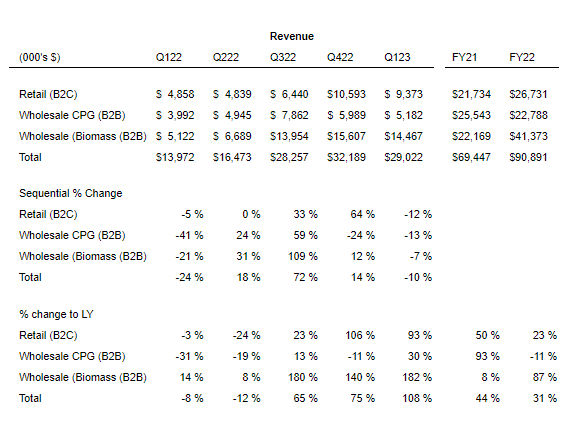

- Net Sales of $29.0 million increased 108% from $14.0 million in Q1 2022 and down 10% sequentially from $32.2 million in Q4 2022.

- Gross Profit was $12.0 million compared to $2.3 million in Q1 2022 and $10.2 million in Q4 2022.

- Gross Margin was 41%, compared to 17% in Q1 2022 and gross margin of 32% in Q4 2022.

- Adjusted EBITDA2 was $(0.1) million, compared to $(6.4) million in Q1 2022 and $(2.6) million in Q4 2022.

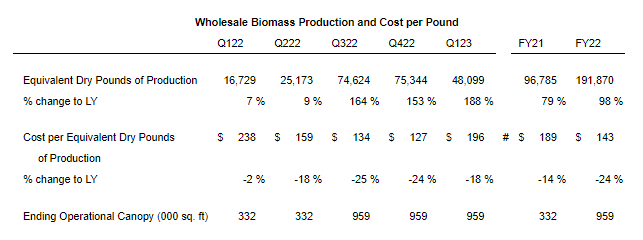

- Cost per Equivalent Dry Pound of Production3,4 was $196 a decrease of 18% compared to the same period last year and up 54% sequentially versus Q4 2022, which was expected due to seasonality.

- Equivalent Dry Pound Production3 was 48,099 pounds, up 188% year-over-year and down 36% sequentially, which was expected due to seasonality.

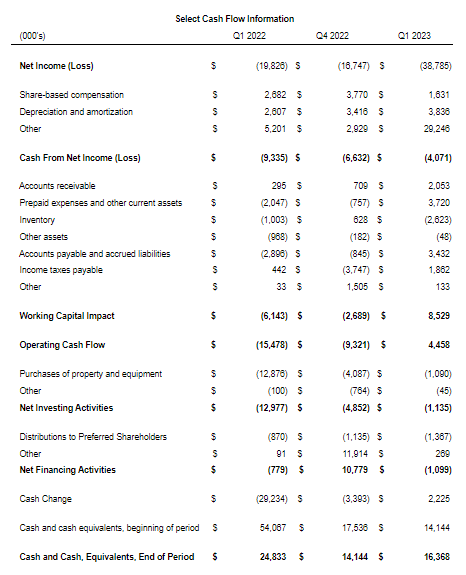

- Cash balance was $16.4 million at quarter-end, up 16% from Q4 2022 quarter end.

Management Commentary

In the first quarter of this year, we achieved free cash flow positive operations one quarter ahead of our guidance. This performance signals that we have crossed a critical threshold in our operations, one that will hopefully lead to increasingly stronger cash flow generation in the months and years ahead.

Kyle Kazan, Co-Founder, Chairman and CEO of Glass House

Kyle Kazan, Co-Founder, Chairman and CEO of Glass House

Kazan added, “we also exceeded our production, revenue and margin guidance for the quarter and narrowed our Adjusted EBITDA2 loss to $0.1 million versus a $2.6 million loss in Q4. Collectively, our performance in the first quarter of 2023 continues to demonstrate that our unique business model has significant competitive advantages that we are just beginning to unlock, which we expect will lead to tremendous growth in both revenues and profitability in the future along with driving substantial value for shareholders.”

“We are increasingly optimistic about future pricing trends based on the latest results in our business as well as what we are seeing across the industry in California relative to capacity and licensing renewals. From June 2022 through the end of April, we estimate licensed California cultivation capacity has fallen by more than 16 million sq. ft. of canopy representing about a 21% reduction in acreage under cultivation.”

“In summary, we continued to execute well against our strategic priorities in the first quarter of this year, driving significant growth and hitting several key profitability milestones including reaching positive free cash flow1. We are consistently demonstrating the durable competitive advantage of our vertically integrated model.”

“I’d like to once again extend a warm invitation to all shareholders to attend Investor Sesh 2023, where investors can tour our unicorn greenhouse facility, ask questions directly to Graham and me along with the rest of our talented C-Suite, and join our annual general shareholder meeting. It will be held on Friday, June 23, at our SoCal Farm in Camarillo, CA from 9:00 AM to 4:00 PM Pacific Time. Transparency is part of our name, and our culture of transparency is reflected in our desire to personally meet and provide tours to our loyal investor base.”

First Quarter 2023 Operational Highlights

- Glass House Brands Announces the Closing of $4.7 million Series C Preferred Stock Offering

- Glass House Brands to Attend the 25th Annual ICR Conference, Announces Preliminary Q4 2022 Financial Results

- Glass House Brands Expands Retail Presence with New Farmacy Dispensary in Santa Ynez

- Glass House Brands Congratulates the Weldon Project and Mission [Green] on the Release of Medical Cannabis Prisoner Luke Scarmazzo

- Glass House Brands to Webcast Live at VirtualInvestorConferences.Com on February 23rd

- Glass House Brands to Host Fourth Quarter and Year End 2022 Conference Call on March 13, 2022

- Glass House Brands Announces Plans for Further Expansion of Cannabis Cultivation Capacity at its SoCal Farm

- Glass House Brands to Participate in the 35th Annual Roth Conference to be Held March 12-14, 2023

Subsequent Events

- Luke Scarmazzo Joins Glass House Brands as Lead Brand Ambassador for NorCal Following his Recent Release from Prison

- Glass House Brands Closes Turlock Natural Healing Center Dispensary Acquisition

- Glass House Brands to Hold 2nd Annual Investor Sesh on Friday, June 23rd

- Glass House Brands Summary of Upcoming Events – Q1 Earnings Call, Attendance at Canaccord Global Cannabis Conference, Investor Sesh 2023

Media Highlights

- Recently Released Luke Scarmazzo Talks Cannabis Advocacy: ‘I Served 15 Years In Some Of America’s Worst Prisons’

- Glasshouse Brands Ranked in FT’s Top 125 Fastest Growing Companies in 2023

- Advisor Shares Presents: 4/20 Cannabuzz Podcast with Kyle and Graham

- The Big Myth About Growing Cannabis: Cannabis is Really Hard to Grow Consistently at Scale

- Glass House Brands Continues to Drive Down Costs to Remain Competitive in California Cannabis

- 7 Years After Legalization, Why Licensed Cannabis Sellers Still Face Stiff Competition From Illicit Market

- CEO Kyle Kazan & CCO Graham Farrar of Glass House Brands | Cannabis Talk 101

- What Law Enforcement Wants You to Know

Q1 2023 Financial Results Discussion

Net revenues for Q1 2023 were $29.0 million, 108% growth versus Q1 2022 and a 10% sequential decline versus Q4 2022 primarily driven by seasonality. This result was at the high end of our Q1 guidance of $27 million to $29 million.

Wholesale biomass revenue of $14.5 million increased 182% versus Q1 2022 and was down 7% sequentially versus Q4 2022. In the quarter, product sold increased 179% year-on-year to over 49,923 pounds of equivalent dry weight.3 The increase in weight available for sale was driven by a 188% increase in production versus last year to approximately 48,100 pounds as a result of incremental production from the Company’s SoCal farm.

Retail revenue in Q1 of $9.4 million increased 93% year-over-year but declined 12% on a sequential basis. The year-over-year increase was primarily a result of incremental revenues from four retail locations we acquired in Q3, the new Farmacy in Isla Vista that opened in mid-December and a new Farmacy in Santa Ynez that opened in the first half of January. For Q2 earnings, our retail footprint will include ten dispensaries with the opening of the NHC Turlock store in late April. Excluding the impact of the excise tax change on January 1, 2023, when retailers began collecting excise tax which resulted in lower revenue, revenue is estimated to have declined 2% sequentially.

Wholesale CPG revenues were $5.2 million, an increase of 30% compared to the prior year and a 13% decline sequentially, ahead of our guidance of down 20% sequentially. The retail credit environment continues to be very challenging, but we were able to navigate this better than anticipated. Discounting is still higher than we’d like to see but has remained relatively stable over the past six months and is significantly improved from a year ago. During Q1, discount as a percent of gross sales was 21%, up slightly from 19% in Q4 but well below the 42% we experienced in Q1 22.

Consolidated gross profit was $12.0 million, or 41% of net revenues, compared to $2.3 million, or 17%, in Q1 2022 and $10.2 million, or 32% in Q4 2022. This is the highest gross margin percent since Q2 2022 which was the last quarter before wholesale prices began their large decline. Importantly, gross margin in each of our three business lines was flat or showed improvement on both a sequential and year-over-year basis.

The sequential increase in gross margin was primarily due to a 23% sequential increase in the average wholesale biomass selling price which rose to $290 per pound. Other factors aiding gross margin improvement were a ten-percentage point increase in retail gross margins from Q4 22 and a 33 percentage point sequential increase in CPG gross margins to 18%. The improvement in retail gross margin was expected. As we mentioned in our Q4 22 earnings call, retailers have been responsible for collecting and remitting excise tax to the state since January 1st of this year. This duty previously belonged to distributors. With this change, the cost of inventory to retailers is reduced by the amount of the excise tax and as a result it is no longer included in revenue but is charged to the consumer as a tax. This does not change the total gross margin dollars collected but reduces inventory cost and revenue by the same amount and results in a higher gross margin by about 10 percentage points. The improvement in CPG gross margin was influenced by two key factors. Our fourth quarter was negatively impacted by several one-time items related to the Plus relaunch and heavy discounting related to the Allswell launch. In addition, we have fully implemented a disciplined sales and operating process that tightly links the sales and production forecast at the item level to ensure better control of inventory levels.

General and administrative expenses were $11.4 million for the quarter compared to $13.9 million in Q4 2022. The $2.5 million reduction was primarily attributable to stock compensation which decreased by $2.1 million to $1.6 million. No new grants were given in the first quarter compared to the fourth quarter, which contained several year-end adjustments. We expect this number to increase in subsequent quarters. The remainder is due to a reduction in bad debt expense. In Q4 22 we incurred bad debt expense of $0.6 million related to Plus receivables from the acquisition.

Sales and marketing expenses were $0.7 million, down 25% year-on-year and 24% sequentially as we continue to be choiceful about where we invest in marketing. Professional fees were $1.5 million, down 42% year-on-year and down 20% from Q4 2022. We have significantly reduced our reliance on outside legal and consulting resources over the last 6 months. We will continue to look for areas where we can further reduce our expenses both in professional fees and general and admin expenses. Our plan all along has been to limit growth in SG&A spending as we increased revenue to improve cash flow and profitability.

Depreciation and amortization in Q1 2022 was $3.8 million, up $0.4 million from Q4 due to the effects of capex spending in the fourth quarter of 2022 for both our SoCal Farm and the Isla Vista and Santa Ynez dispensaries.

During the quarter, the company recognized a non-cash impairment expense of $23.0M for Goodwill and Intangible Assets in its Wholesale CPG business segment related to the Plus Products Holdings acquisition. The impairment was triggered by a decline in the outlook for revenue and profit for the Wholesale CPG business segment which resulted in the fair value of the business segment being less than the carrying amount. This difference created the impairment charge in the quarter.

Adjusted EBITDA2 loss was $(0.1) million in Q1 2023, compared to adjusted EBITDA loss of $2.6 million in Q4 2022. The increase was driven by top line growth, gross margin expansion and improved management of operating expenses. Please note, the Q4 22 adjusted EBITDA2 result included the incremental manufacturing costs and inventory write offs associated with the Plus relaunch and the bad debt expense associated with the Plus distributor move in Q3 22.

We generated $4.5 million of cash from operations in Q1 23 versus cash usage from operations of $9.3 million in Q4 22 and $15.5M Q1 22. In Q1 our cash impact from net income improved to ($4.1) million from ($6.6) million in Q4. In addition, working capital benefited by $5.6 million because there was no income tax paid in the quarter. Recall in Q4 22, we paid our state and federal taxes for fiscal year 2021. In addition, we had favorable working capital broadly within the Q1 23 quarter.

Capital spending was $1.1 million in Q1 compared to $4.1 million in Q4 as the capital expenditures associated with the Isla Vista and Santa Ynez stores were complete in Q4 and the capital expenditures associated with the SoCal farm dropped to $1 million vs. $2.5 million in Q4.

2023 Outlook

The Company is providing the following guidance for 2023 based on the strength of our first quarter results and current trends from the first quarter of 2023.

2023 Cash Flow and EBITDA2

With the improved wholesale pricing which we assume maintains for the balance of the year, we expect to have positive operating cashflow and positive adjusted EBITDA in Q2 and for each quarter the rest of the year.

Q2 2023 Outlook

We expect revenue to be between $38 million and $40 million. The increase vs. Q1 23 is being driven by the seasonal increase in production of biomass due to higher sunlight levels in Q2 relative to Q1 and our assumption CPG and Retail revenue will collectively be flat relative to Q1 due to the continued difficult retail environment. Our average selling price for wholesale biomass is projected at $325 per pound based on trends through the early part of May.

We expect consolidated gross margin percent to be in the mid-40s versus Q1’s 41% because of the higher seasonal production in cultivation which we project to be 75,000 pounds, leading to an expected reduction in cost of production to $150 per pound in Q2 from $196 in Q1. The $150 pound level is a 5% reduction from Q2 22, and the projection of 75,000 pounds produced is a 198% increase vs. Q2 22.

In addition, we expect adjusted EBITDA2 to exceed $5 million and expect operating cash flow to be similar to Q1 at around $4 million.

We expect capex to be similar to Q1 at approximately $1 million.

2023 Fiscal Year

We are maintaining our revenue guidance of $160 million for 2023 but are shifting sales between our segments.5 As a result of the higher pricing in biomass wholesale, we are increasing our wholesale revenue projection to $100 million from $85 million. We are raising our projected average selling price per pound to $330 from $300 and expect it to increase from Q1 through the remainder of the year as the mix of flower produced during the year increases.

We are reducing our CPG revenue guidance to $20 million from $25 million which takes into account our move to a direct distribution model to our owned stores, and results in a reduction in top line revenue as we previously sold CPG to our distributor who then sold to our stores. It also reflects the continued difficult retail landscape and our expectation that we will be dealing with significant retailer distress and high levels of account shipping holds during the year.

In addition, we are reducing our retail revenue guidance to $40 million from $50 million because of the extremely competitive marketplace, heavy discounting and our new stores not meeting internal projections.

Finally, for this fiscal year we are raising our biomass production estimate to 315,000 pounds from 310,000 pounds, but raising our cost of production3,4 estimate to $140 per pound from $130. Given the state of the wholesale biomass market, with strong demand and improving pricing, we have increased our emphasis on maximizing production, which is reflected in our increased production estimates. In parallel we are working on a number of operational improvements to processing, which we believe will have long term net benefits, but which have short term efficiency costs. Until we see those improvements translate, we are being slightly more conservative on our full year production costs. We remain confident in our long-term cost target of $100 per pound. The new guidance represents a 64% increase for production and a 2% reduction in costs vs. FY 2022. Note that we typically produce roughly 60% of the year’s total biomass volume in the second half, and we expect this to hold true in FY 23. In FY 22, 78% of our biomass was produced in the second half of the year when production costs are at their lowest, biasing the annual cost of production number downwards. In the second half of 2023 we now anticipate the cost of production3,4 will be below $120 per pound versus our original projection of below $110 per pound. This is still an 8% decrease vs. the same period in 2022.

None of the above guidance includes any impact from the potential greenhouse expansion discussed earlier.

Financial results and analyses will be available on the Company’s investor relations website (https://ir.glasshousegroup.com/) and SEDAR (www.sedar.com).

Unless otherwise stated, all results are in U.S. dollars.

Conference Call

Conference Call

The Company will host a conference call to discuss the results on today, May 15, 2023 at 5:00 p.m. Eastern Time.

Webcast: Click here

Dial-In Number: 1-888-664-6392

Conference ID: 77602802

Replay: 1-888-390-0541

Replay Code: 602802 #

(replay available until 12:00 midnight Eastern Time Monday, May 22, 2023)

Non-GAAP Financial Measures

Glass House defines EBITDA as Net Loss (GAAP) adjusted for interest and financing costs, income taxes, depreciation, and amortization. Adjusted EBITDA is defined as EBITDA excluding share-based compensation, stock appreciation rights expense, loss (income) on equity method investments, change in fair value of derivative liabilities, change in fair value of contingent liabilities, acquisition related professional fees, and non-operational start-up costs.

EBITDA and Adjusted EBITDA are presented because management has evaluated the financial results both including and excluding the adjusted items and believe that the supplemental non-GAAP financial measures presented provide additional perspective and insights when analyzing the core operating performance of the business. Such supplemental non-GAAP financial measures are not standardized financial measures under U.S. GAAP used to prepare the Company’s financial statements and might not be comparable to similar financial measures disclosed by other companies and, thus, should only be considered in conjunction with the GAAP financial measures presented herein.

The Company has provided a table above that provides a reconciliation of the Company’s net loss to Adjusted EBITDA for the three months ended March 31, 2023 compared to three months ended March 31, 2022 and three months ended December 31, 2022.

Footnotes and Sources:

1. We define Free Cash Flow as net cash from operating activities minus capital expenditures.

2. EBITDA and Adjusted EBITDA are non-GAAP financial measures that are not defined by U.S. GAAP and may not be comparable to similar measures presented by other companies. Please see “Non-GAAP Financial Measures” herein for further information and for a reconciliation of such non-GAAP measures to the closest GAAP measure.

3. Includes all dry production (flower, smalls and trim) plus equivalent dry weight for wet weight and fresh frozen not converted into dry weight by the Company.

4. Cost per Equivalent Dry Pound of Production, is the application of a subset of Costs of Goods Sold for cannabis biomass production (including all expenses from nursery and cultivation to curing and trimming – the point at which product is ready for sales as wholesale cannabis or to be transferred to CPG) applied to the Company’s metric of dry production which includes all dry production (flower, smalls and trim) plus equivalent dry weight for wet weight and fresh frozen that is not converted into dry goods by the Company.

5. The Company has provided guidance that 2023 revenues will reach $160 million. The statement assumes the following in revenues from each source: 1) Annualized wholesale biomass sales of $100 million; 2) Annualized retail revenues of $40 million; 3) Annualized wholesale CPG revenues of $20 million.

About Glass House

Get ahead of the crowd by signing up for 420 Investor when it becomes available again. It’s the largest & most comprehensive premium service for cannabis investors since 2013.

Get ahead of the crowd by signing up for 420 Investor when it becomes available again. It’s the largest & most comprehensive premium service for cannabis investors since 2013.

MJ Shareholders

MJShareholders.com is the largest dedicated financial network and leading corporate communications firm serving the legal cannabis industry. Our network aims to connect public marijuana companies with these focused cannabis audiences across the US and Canada that are critical for growth: Short and long term cannabis investors Active funding sources Mainstream media Business leaders Cannabis consumers

No comments so far.

Be first to leave comment below.